Full warning, similar to Armstrong Flooring (AFI), this could be a terrible idea, it has significant red flags and is highly speculative.

LMP Automotive (LMPX) is a micro-cap (~$45MM market cap) that came public in late 2019 with a car subscription model where users could rent a car month-to-month, positioning itself as splitting the difference between a short-term car rental and a traditional car lease. LMPX then put an online dealer/mobile app business model spin around it to market the stock. In 2020, LMPX became a bit of a meme stock, briefly trading up alongside other e-commerce car dealers like Carvana, but then crashed as they were unable to source cars economically to run their subscription model. Instead, the company pivoted to be a traditional car dealership rollup business and went on a debt fueled acquisition spree in 2021. LMPX finished the year with 15 new car dealerships and 4 used car dealerships across 4 states. On 2/16/22, the company said they were unable to secure new financing for their previously announced but not yet closed acquisitions (7 of them!) and quickly pivoted to pursuing a sale:

Sam Tawfik, LMP’s Chief Executive Officer, stated, “The Company intends to terminate all of its pending acquisitions in accordance with the terms of their respective acquisition agreements, primarily due to the inability to secure financial commitments and close within the timeframes set forth in such agreements.”

“The Board of Directors believes that LMP’s current stock price does not reflect the Company’s fair value. Given the record M&A activity in our sector and multiples being paid for these transactions, LMP’s Board of Directors has directed management to immediately pursue strategic alternatives, including a potential sale of the Company.”

The stock closed at $5.25/share on 2/16, it now trades for ~$4.25/share.

Putting aside terminal value questions (auto OEMs bypassing dealers, electric cars needing less maintenance), car dealerships are fairly high cash flowing business and were big covid beneficiaries. There is a lack of supply (nationwide, dealership inventory is ~1/3rd of normal, going to take a while to normalize) that has raised prices and reduced the need for car salespeople (dealerships have been slow to rehire those laid off during the pandemic) as more people browse online and the low inventory has all but eliminated haggling. Car owners are also holding onto to their cars longer creating more high margin service revenue. Some of these covid changes may be lasting, many dealers talk about inventory being permanently lower as dealers become more of a distribution center and less of a place where people walk the lot to find the car they want, they've already decided on the specs online before going to the dealer.

There are thousands of dealerships across the country, they're reasonably liquid assets that change hands regularly (similar to why I like REIT special situations, the assets are fungible and there's a large pool of buyers). Here, there are 7 large publicly traded dealership groups (KMX, LAD, PAG, AN, ABG, GPI and SAH, but only ~10% of all dealerships) and many other large private ones. The windfall profits of the last few years has prompted the larger public players to do a lot of M&A, rolling up this fragmented market. While large dealership groups are thriving, many smaller dealerships are struggling to source inventory and are at risk of failure, in order to press their scale advantages, the big are getting bigger. Awkward long way of saying, I don't think LMPX will have trouble finding buyers for their dealership assets, but it is more a question of price.

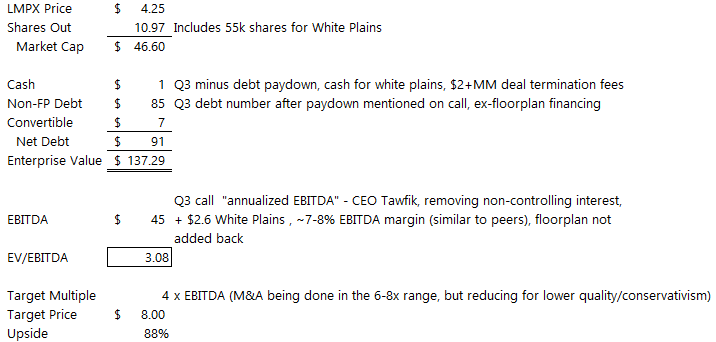

Given the rapid rollup nature of LMPX, nailing down the valuation causes a bit of brain damage to work through the financials, here's what CEO Sam Tawfik said in the Q3 earnings call:

Our third quarter annualized run rates excluding the acquisition we closed this quarter, which we expect to be immediately accretive to income this quarter are $565 million in revenue, and $47.6 million in adjusted EBITDA.

The acquisition referenced above is the White Plains Chrysler Dodge Jeep Ram Dealership that closed in October, purchased for $19.2MM that was estimated to generate $2.6MM in 2022 EBITDA.

Then in the company's annual letter on their website, Tawfik provides:

We completed the acquisition of our contracted White Plains, New York Chrysler Dodge Jeep Ram in the early fourth quarter using approximately $5 million in cash from the company’s balance sheet, 55,000 shares of common stock and $1.3 million in cash from our existing credit facility. This acquisition will be immediately accretive to earnings in the fourth quarter of this year. As a result of this year’s acquisition activity, the company currently owns 15 new vehicle franchises, operates 4 pre-owned stores across 12 rooftops in 4 states which generate over $600 million in annualized revenue.

Later:

We intend to pay down our existing term debt by approximately $11 million in the fourth quarter of 2021, resulting in a balance of approximately $85 million, of which the company allocates $53 million to its real-estate holdings and $32 million to its dealership blue sky purchase debt. Essentially at the current pace of cashflow generation, if we choose, the company can extinguish its current blue sky debt in less than a year.

Adding it up together:

Risks/Red Flags:

- Obviously, top of the list, LMPX went on a crazy acquisition spree in 2021 and couldn't raise capital to complete them (credit conditions have tightened slightly this year, but still pretty open). Most of these deals included a combination of debt and stock, struck when the stock was $15-$17, by the time it came to close these transactions the air was being let out of the growth balloon, the stock was $7 and the window to raise capital closed on LMPX. Buying dealerships at 7x EBITDA while the stock trades well below that doesn't make much sense. It could be nastier than that simple explanation under the hood, but the Q3 numbers look fairly decent, this is a mess but was at least cash flow positive during the last reported quarter.

- Tawfik owns approximately 35% of the company, he appears to be the sole decision maker and doesn't seem to have a strong board around him. There are a number of related party transactions, none appear overly egregious but in total they don't look great, plus in October, Tawfik bought a company plane for himself only a few short months before it all fell apart. His biography includes founding Telco Group which was sold to Leucadia back in 2007 for $160MM and also founded PT-1 Communications which was sold to Star Communications in 1998 or $590MM. Presumably he's not totally incompetent but might have just gotten caught up in the market hysteria last year.

- Tawfik has been selling a small amount of shares regularly as part of a 10b5-1 plan, I'm not an expert on these insider selling plans, not sure if they can be cancelled halfway through, but it is not a great look if you think the stock is materially undervalued.

- LMPX reports EBITDA per share versus enterprise value, that's always a red flag for me as it is intentionally comparing apples to oranges.

- Their current term loan matures in March 2023, so they've got a little time to get this process done and less of a forced sale than AFI.

Disclosure: I own shares of LMPX