Oramed Pharmaceuticals (ORMP) (~$85MM market cap) is a biotechnology company that has a platform designed to reformulate injections/vaccines into orally administered drugs. Their furthest along asset is ORMD-0801, orally administered insulin for diabetes patients, it recently did not meet its primary or secondary end points in their Phase 3 trial. Previously, Oramed had been guiding to a 2025 anticipated FDA approval for ORMD-0801, given this sudden failure, the stock naturally dropped considerably on the news. Then on 2/9, the company announced they were "examining the Company's existing pipeline and conducting a comprehensive review of strategic alternatives focused on enhancing shareholder value." In addition to the diabetes trial, Oramed does have an ongoing Phase 2 trial for ORMD-0801 in patients with NASH, a liver disease without an approved FDA treatment. Lastly, Oramed owns 63% of Oravax, a joint venture that is pursuing an orally administered COVID-19 vaccine and other applications of an oral vaccine.

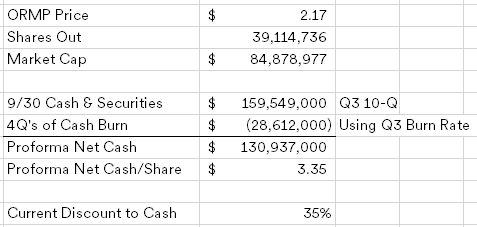

Doing the same math as MGTA, below I took the 9/30 cash and subtracted four quarters of their cash burn (including the $1MM/quarter in interest income) since they're earlier in their busted biotech lifecycle, i.e. they haven't let go of their workforce (couldn't find the employee count in their filings, but Oramed only has 16 employees on LinkedIn) and haven't shutdown their other trials. On the plus side, they only have a minimal lease obligation here, making it a bit of a cleaner balance sheet.

Disclosure: I own shares of ORMP

Another interesting one. It’s better that they announce strategic alternatives before it’s the last resort. (Theoretically)

ReplyDelete$STSA (which MDC mentioned before) is interesting because they had a drug that failed both co-endpoints of reducing different types of pain at 2 hours but at 3+ hours there was a good effect. And of course if the drug is worthless you can probably still make money. Interesting Pabrai coin toss. Announced strategic alternatives but will file an NDA later this year.

Thanks - I lost track of that one to be honest. I need to take another look at it.

DeleteORMP run by fraudster, maybe they take another Israeli fraud to market or find a real co in their network, no cash coming back to shareholders, no stewardship here

ReplyDeleteAny context you can provide? Examples?

DeleteI met the CEO in 2017/2018 when he was leveraging the Israeli ambassador's network to raise money, mother son team at the core of the co..... their primary product was a FAKE MOA insulin pill (no matter how you coat it the insulin is not absorbed via GI there are no transporter proteins for it instead it just breaks down by enzymes in GI) + as they hyped the co they cited publications in esoteric scientific journals and provided clippings but were never published in the actual journals themselves........run run run run run run run run

DeleteThanks, I appreciate the thoughts.

DeleteAgree with the above. Had the stock several years ago, they were touting a drug study on the insulin pill. It finally came out and there only a few people in the study. Stock went to the upper 20’s on the hype. It opened that morning up a couple of points and when everyone realized it was bogus, it dropped like a rock. Fortunately got out before I lost my shirt. I think at the time the big competitor was MannKiind.

DeleteSpeaking of liquidations...can't recall whether someone else mentioned this, but URF.ax, a ridiculous ZIRP-era product listed in Australian that bought up and renovated a lot of resi property in the New York area, has effectively gone into liquidation. It was insane from the beginning because a lot of the portfolio is (multimillion-dollar) single family homes so there was very little economy of scale. They streamlined the ops and capital structure and have taken on a new local manager to handle the properties and try to sell them down starting, most likely, with the best of them.

ReplyDeleteNAV is ~.60 a share; price, which has been slowly rising, is ~half that. Manager incentives kick in once .40/share has been returned to holders. That hurdle grows at 8% annual compounded, which is a decent alignment. RE liquidations can be endless affairs--just look at DCI.L--but these aren't suburban offices or raw land in Crete. I'm familiar with many of the Brooklyn and Jersey City properties, and they're decent.

Co management is seeking permission to buy back up to 25% of the shares outstanding, which is both good and bad; obviously accretive, but also might end up extending the fund life and concentrating control, potentially.

Anyway, I've been buying in the 27 cent range; it seems to me a pretty good risk/reward.

Liquidating distributions should be treated as returns of capital, but are brokerages like Interactive Brokers smart enough to not withhold taxes? Australian withholding rates on dividends for non-residents are 30%, and doing the tax reclaim would be an expensive hassle if they screw things up.

DeleteIB pretty good (not perfect!) in my experience about getting it right (IIRC, they didn't withhold on the RKN special last year). But next-year plan seems to be recycling disposition proceeds into buybacks, driving NAV growth. I assume distributions follow and (depending on particulars) would probably sell on a decent post-announcement pop if I can do it at LT gains rate (if there is a gain!). Depends on what stub is, etc., but last puff on these things often not worth it.

DeleteSince you mentioned the very last puff, have you looked at NEW.AX? Management expects to return 0.08/sh net of expenses, and it looks like it's possible to buy at 0.065. If it winds down by October as expected, the IRR is ~30% (possibly more, since management estimates tend to be conservative in liquidations).

DeleteOoh thanks! Never looked at it; will do so.

Deletere: NEW.AX: latest presser mentions that while NAV is $0.08, the latest future capital return estimate was $0.205 and they distributed $0.135 since. And that the NAV is different because of 'the contingent nature of certain liabilities which are not yet reflected in the weekly NAV estimate'. So looks more like $0.07 to me a first glance (?). I could be wrong though.

DeleteThanks for pointing that out! I was skimming the PR too quickly. I did take a closer look though, and they seem to be conservative in their estimates. The most uncertain thing in their contingent liabilities is the US tax liability, which is estimated to be between 9-13MM USD, and they've reserved the full 13MM. If the final liability lands at the midpoint of the range, then that amounts to an extra ~0.01 AUD/sh. No position in NEW, btw. Just thought it was potentially interesting.

DeleteThanks for the interesting idea. Have you looked at MEI Pharma? It discontinued its primary product in last December and initiated a strategic review. MEI hired Torreya Partners as financial advisor and the decision is pending for 2 months, can be realized at anytime. MEI has $124M of cash by EOY22 and has no debt and the current market cap is only $42M.

ReplyDeleteThere is just one thing I am unsure of: there is a $64M of long-term deferred revenue as a result of some R&D agreement with another biotech company. Not sure whether I should subtract this from cash. Quote from 10k: this $64M "is a unit of account under the scope of ASC Topic 808, and is not a performance obligation under Topic 606."

Does anyone has an idea of what this is? Thanks!

They seem on the fence, they did hire Torreya Partners, but they also have two clinical data readouts they anticipate receiving towards the end of the year which will sway what path they take. I typically like ones that have fully given up. But its an interesting one to add to the watchlist.

DeleteInteresting thinking about the risk-reward differences between the near cinch biotech liquidations with 25-40% IRRs (or there about) vs the biotech netnets that trade at a substantially greater discount to cash and some of the netnets having the potential to become multibaggers because their pipeline may be worth much greater than nil.

ReplyDeleteTrue - why not a basket approach with a mix of both? The latter is tougher for me as a biotech tourist, but I do like the optionality.

DeleteAnyone looking at GRPH? I have done no work on it, but someone I know who likes these type of plays called it out to me a couple weeks ago.

ReplyDeletehttps://ir.graphitebio.com/press-releases/detail/85/graphite-bio-announces-process-to-explore-strategic

I did a little work on that one, similar to MGTA, they had an adverse event (on their very first patient) so the IP might not be worth much. But I do like the size of their cash hoard, makes it more attractive for reverse merger candidates versus some of the super tiny busted biotechs. GRPH could do a special dividend alongside a reverse merger, similar to SESN. Get sort of the best of both worlds, most of your cash back but some upside potential.

DeleteDid you have a look at Xbiotech? Cash burn is $30-40m a year. EV is $-120m. So you could buy, and hope their current treatments that are in trial will pay off, or in a few years time they do a strategic review as well? Given cash burn and large discount to net cash.

ReplyDeleteBarely any info out on the company. And they do have some revenue occasionally. Interestingly they did a large buyback and paid a special dividend 2020 and 2021 respectively.

After looking at glassdoor reviews I get why it is so cheap:

Delete"There are no advantages to working here, unless your goal in life is to eclipse Theranos in scientific malfeasance, unethical behavior, and moral corruption — then this is the place for you. XBiotech epitomizes all the worst of biotech and absolutely none of its periodic brilliance."

10k looked good w/r/r this thesis: Low burn, not too much dilution, ample cash and short term deposits remaining. Any updated views based on it?

ReplyDeleteW/r/t* (sorry for typo)

DeleteNo updated views from my end. I do appreciate others chiming in on a fraud fear here, but my position is sufficiently small enough that I'm going to hold until something happens.

Deletehttps://www.sec.gov/ix?doc=/Archives/edgar/data/1176309/000121390023034728/ea177755-8k_oramed.htm

ReplyDeleteOddly, Ben Shapiro is joining the board and owns a 4% stake in the company. Doesn't sound like they plan on liquidating by the commentary in the press release.

I sold today. Don't appear to be liquidating and based on earlier comments in the thread, the founding team here doesn't have the best reputation.

Delete