Typically, I don't like to write about stocks that I don't own but I'm going to break that soft rule here, as mentioned in the Year End post, I sold my shares in Advanced Emissions Solutions (ADES) ($59MM market cap). My original post outlining the thesis from November 2021 is here, as usual, the comment section is worth going through for a blow-by-blow of the events.

This afternoon, ADES published a press release announcing their merger with Arq Limited had been completed. That required a double take and a quick click since the merger as originally constructed required a shareholder vote to complete, and no such vote was held.

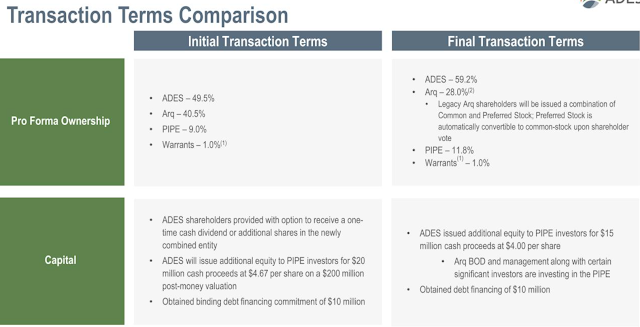

To take a step back, in May 2021, ADES announced it was pursuing strategic alternatives as the run off in one segment was generating a lot of cash, but that business was coming to an end due to the expiration of a tax credit, leaving just their Activated Carbon business (Red River plant) which is subscale for a public company. According to the background section in the original deal's S-4 filing, ADES received several non-binding indications of interest from private equity firms shortly after publicly announcing a process for their remaining Activated Carbon business for between $30-$50MM. However, ADES flipped to being a buyer and in August 2022, finally entered into an agreement with Arq Limited for a reverse merger where ADES would acquire Arq for cash and stock. It was a very SPAC-like deal (here's the SPAC deck) with a pre-revenue startup and rosy revenue outlook several years out. Shareholders who were expecting a liquidation type transaction revolted, sending the shares from $6.41 immediately prior to the deal announcement (to be fair, it had spiked over the previous week after ADES management indicated a deal was near on their Q2 earnings call) to a $3.86 on the close, then drifting all the way down to $2.20/share in December. For context, as of 9/30 the company had $86MM of cash or $4.50/share, if they sold the Activated Carbon business to one of the PE firms, shareholders could have netted somewhere in the area of $6.50/share. Much lower than I originally penciled out, but well ahead of where shares trade today.

With that value discrepancy, you'd expect an activist to come in and attempt to break the deal, force a quick sale of the Activated Carbon business, distribute all the cash and reap a nice tidy profit. However, that was impossible because ADES has a rights agreement preventing anyone from crossing the 5% ownership threshold in order to maintain their NOLs and tax credits. That 5% ownership limit in combination with the small market cap prevented most funds from owning shares (its individual investors who are getting screwed here). In a strange twist, the original transaction with Arq Limited would qualify as an ownership change, therefore eliminating the NOLs and tax credits, but the rights agreement protecting those tax assets was still in place. Despite that, there was some hope that shareholders would vote the deal down (like MTCR that was discussed in my SESN post comments) or it would be terminated before to save the embarrassment, forcing the company into a liquidation.

That brings us back to today, ADES recut the merger with Arq presumably to circumvent the shareholder vote by issuing a new series of preferred shares (this kind of rhymes with the shenanigans over at AMC with the APE preferred shares) to Arq shareholders as consideration.

The preferred shares feature a 8% coupon and are convertible to common stock at a $4/share conversion price if approved by common stock holders. Common stock holders have no reason not to approve the conversion, saves the 8% coupon the company can't afford (it will be cash flow negative for the next couple years, even under their rosy projections) and it would convert at an above market price. The debt financing is also to a related party, a board member of Arq (will also be on the new ADS board) that pays 11% cash coupon, plus a 5% PIK.

While the deal is optically better for ADES shareholders (not saying much, presumably does preserve the tax asset, but questionable whether the combined company ever generates significant taxable income), it likely would still get voted down, after hours trading reflects this as well, shares were down ~16% as of last check. Hard to speculate on motivation, but management owns little stock and probably wants to keep their well paying jobs. Apologies to anyone that followed me into this situation, I hope I'm missing something. None of this smells right.

Disclosure: No position

Criminal. I would love to see the SEC come in to kick the tires on this one.

ReplyDeleteCriminal might be a bit far, but certainly unethical.

DeleteHave you looked at what the new team at ADES is working on? Just wondered if you kept tabs on it, seems like their plan is starting to come together but could understand steering clear under the once burned twice shy rule.

ReplyDeleteI'm steering clear, but I'll take a look at the current developments when I get a chance, thanks for pointing it out.

Delete