Star Holdings (STHO) (~$225MM implied market cap) is the upcoming spinoff of the merger of iStar (STAR) and Safehold (SAFE) targeted to be completed on 3/31/23. Similar to other real estate spinoffs, STHO will be stuffed with legacy assets with a stated strategy to monetize the portfolio over time and return sale proceeds to shareholders.

iStar was a commercial mREIT prior to the great recession, during '08-'09 many of their commercial mortgage loans went bad and the company ended up foreclosing on various property types across the country. In the years since, they've run off much of that legacy portfolio (I previously owned it for the legacy assets) and then several years back launched a new ground lease strategy under the Safehold (SAFE) banner, a REIT that is externally managed by iStar. As the SAFE strategy succeeded in the low rate environment (a ground lease is typically 99 years, about the longest duration asset you'll find) and iStar's legacy portfolio ran off, there was little need to maintain two separate public companies with related party arrangements. iStar with its management contract and SAFE shares was basically an asset backed tracking stock of SAFE. Last August, iStar and SAFE announced a merger transaction where SAFE would internalize management and iStar would spinoff its non-ground lease assets into STHO. Similar to other real estate spins (SMTA, RVI, etc), the new combined SAFE will be the external manager of STHO.

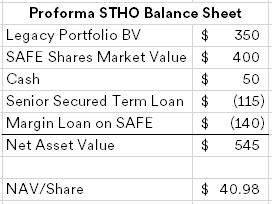

As usual in spinoffs now, iStar will be receiving a dividend back from STHO, the use of funds is to pay down iStar's debt and leave primarily just SAFE shares to then swap for new SAFE. In order to facilitate that dividend, STHO is receiving $400MM in SAFE shares that they will then take a $140MM margin loan out against and send that, plus a $115MM term loan collateralized by all of STHO's assets back to iStar. The term loan will amortize down quickly as all cash above $50MM will sweep to pay down principal and the margin loan will be in place at least 9 months per a lockup agreement on STHO's SAFE shares. The proforma STHO looks something like this (note, the STHO share count will be approximately 13.3 million, or 0.153 shares for every STAR share):

The trickier, and possibly scarier part of STHO is the SAFE shares, as mentioned, its basically a perpetual bond masquerading as an operating company. But with the rate curve substantially inverted, the market is pricing in quite a few rate cuts that would be beneficial to SAFE shares.

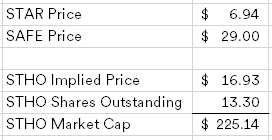

On March 17th, iStar put out a press release estimating the consolidation ratio with SAFE (it will be finalized immediately prior to the merger using a VWAP calculation) at 0.15 shares of SAFE for each share of STAR. Using that ratio we can back into the implied price of STHO:

Management Fees and Expense ReimbursementsWe do not maintain an office or employ personnel. Instead, we rely on the facilities and resources of our manager to conduct our day-to-day operations.We will pay our manager an annual management fee fixed at $25.0 million, $15.0 million, $10.0 million and $5.0 million in each of the first four annual terms of the agreement, and 2.0% of the gross book value of our assets thereafter, excluding the Safe Shares, as of the end of each fiscal quarter as reported in our SEC filings. The management fee is payable in cash quarterly, in arrears. If we do not have sufficient net cash proceeds on hand from sales of our assets or other available sources to pay the management fee in full by the original due date of the management fee, we will pay the maximum amount available to us by the original due date and the remaining shortfall will be carried forward and be paid within 10 days after sufficient net proceeds have been generated by subsequent asset sales to cover such shortfall in full; provided that in no event may such shortfall in respect of any fiscal quarter remain unpaid by the 12 month anniversary of the original due date.

Disclosure: I own shares of STAR and short shares of SAFE (synthetically long STHO)

How much capex will STHO need to spend on the legacy portfolio to make them saleable? How much interest will they pay on their loans? Mgmt fees? Pubco costs? Taxes?

ReplyDeleteAll good questions, maybe too much for a simple back of the envelope write-up. It all comes down to the speed of monetization, many of the legacy assets are in various stages of marketing. They do mention some capex needs in their form 10 related to Magnolia Green and Asbury Park, but their intention is to sell development sites to third parties to develop, STHO won't be the one doing the heavy lifting. Management fees are laid out above, $55MM over 4 years, escalating down each year. Taxes should be a good problem to have, the spin will be taxable to STAR shareholders, but corporate level tax should be minimal at STHO. They have been selling assets at a slight premium to their book value, but that would mean the NAV is solid and maybe understated, at the current prices I view that as a good problem to have.

DeleteSafe to assume you don't think this spin gives any merit to Klarman/Greenblatt's theory about indiscriminate spinoff selling? I like the thesis, just thinking about buying most post spin so want to make sure I don't miss the party.

ReplyDeleteNo I think has merit. I'll probably buy some more post spin. As I mention, it'll be a c-corp and not a REIT, so there might be some investment mandates that are forced to sell it. If the spin was going to both STAR and SAFE holders you might get more indiscriminate selling, but since these assets have always been apart of STAR and STHO will also still have SAFE exposure, other than formalizing the liquidation strategy, not sure how many STAR holders will indiscriminately sell STHO.

DeleteLooked at it, came to similar conclusions, haven't yet bought. Worry disposition might drag, though I do like the timeline. If spin dynamic hits price, will buy.

ReplyDeleteSugarman a mixed bag, but def better than management at CORR and HCDI, where I've been buying the suspended-payment preferreds. Awful companies, but hard (if questionable) assets and catalysts (especially for CORR) offer some protection. Will see how that works out.

And I assume you're already looking at JNCE?

I didn't pay much attention to JNCE, should I? Have a bias against Kevin Tang.

DeleteDidn't realize that! Very fair; I have watched him from afar. I figured his offer was genuine (though far from certain) because of the extreme discount to cash acquired, and was also somewhat sanguine on the initial combination, though not enough to buy into it (bought AH at $1.37 post-announcement). If you don't like/trust KT, though, a pass for sure.

Deletecan you show me how to compute the implied price for STHO please?

ReplyDeleteI am not smart enough to figure it out.

Thank you.

If I may, using the price used for the write-up: for $6.94 per share of STAR you are getting 0.15 x $29 = $4.35 SAFE shares. So whatever is remaining ($6.94-$4.35=$2.59) must represent the value of 0.153 of one STHO. So implied value of one full share of STHO is $16.93 ($2.59/0.153)

DeleteI was interested until I dug deeper into it. Prior to the spin-off, they sold a handful of cash flowing properties and loans - the $37.7MM retail/entertainment center loan was sold, the $29.4MM Germantown active adult loan was paid off, and the two active adult projects they JV'd with Avenida on (Naperville, IL and Lakewood, CO) were sold. The majority of these proceeds went to effectuate the merger and spin-off, not to the benefit of STHO. It's hard to determine what the operating income is from these assets, but the assets STHO is left with is primarily land holdings and shares of SAFE. The only operating assets left are the Asbury Ocean Club Hotel, the Asbury Hotel, Asbury Lanes, and the golf course operations of Magnolia Green. They also hold two loans, one $6.675MM senior loan on an apartment project which produces interest income, and one $13MM junior loan on a hotel project which is not currently paying interest as the accrued interest has been added to their carrying value. The rest of the real estate value is derived from residential lots at Magnolia Green, commercial sites at Asbury Park (broken project IMO), their Coney Island Bath site and various other land sites. I estimate their remaining real estate to be valued at $290MM. SAFE shares currently trade at $29.50/share - it looks like their ground leases produce approximately $250MM in NOI and looking at their post-spin BS, implies the ground leases, excluding the separate ground lease fund, are currently valued at $5.55B, or a 4.5% cap rate. Maybe not crazy for todays market or NYC, for example, but they also hold ground leases in tertiary markets which would trade at much higher cap rates. Outside of gateway markets, properties subject to ground leases trade at decent discounts. I actually think it's a bad business model to begin with except for select markets. It's especially bad for public shareholders because the ground leases are actually owned in an operating partnership, of which there are two classes - one class that essentially receives the ground-lease payments and another class which receives any proceeds above cost on the sale of any ground lease. These "Caret" units are given to management as incentive pay, as well as sold to other third party investors. The shareholders own the majority of these Caret units at the moment (85%(, but will likely be diluted over time as management as sole control over the issuance of these. Regardless, just stress test it a bit. If the cap rate on the portfolio rises to 5.50%, which in other property types, a 100 bps increase in cap rates from 2022 is already happening, the implied price per share would be $13.50. In addition to the risk of concentration in land holdings and low yielding ground leases, they are going to burn through cash now that most of their assets producing income have been sold and they've only added to costs with their management fees and interest expenses on the margin loan and term loan. I estimate they'll have operating income of $40MM and expenses of $90MM, resulting in a minimum annual cash burn of $50MM. This does not account for any CAPEX that needs to go into the remaining projects to sell them. Everything is riding on fast land sales at carrying values from 2022 pricing in the face of weakening real estate markets, in addition to the value of low-yielding ground leases. I think it's likely land sales will not be quick enough and the ground-lease business will be re-rated by the market (they're essentially loaning money out for 99 year terms locked into with 2-3% bumps, but they need to borrow short term).

ReplyDeleteThanks for thoughtful comment. I need some time to digest it, but don't disagree on the face. But I believe the asset sales did benefit STHO in that they'll have less debt at closing. Either way, the lack of cash flow is an issue, I might decide to close this out and just monitor as the situation develops. SMTA and RVI had several opportunities along their path to make money.

DeleteI'll have to double check, but the assets sales I'm speaking of were not specifically called out, but they were alluded to in the updates in Feb and March, and I confirmed which assets were actually sold by checking local property sales records. My understanding is these sales got them to the threshold they needed to go forward with the merger. Any excess cash from sales would go to STHO, but I didn't think there was much, if any. On the debt, I'm pretty sure the margin loan of $140MM and the term loan of $115MM was locked in. Not sure I have enough conviction to short this, but I'm steering clear and watching from the sidelines. Either way, keep us posted if you dig further or bail on your position. Appreciate your posts and regularly follow the blog.

DeleteI closed it out this morning, small but quick gain. I do appreciate pushback on my posts, I don't have a good rebuttal for your points, they all make sense to me in general. I have enough real estate exposure that I don't need another spin that could tank like so many others recently. I'll keep up with it, I think there will be a better opportunity down the road when the liquidation is cleaner. Thanks again.

DeleteWhere did you see the updates re: the sales / loan paydowns prior to closing? If that is the case and STHO received the proceeds, wouldn't that make it more compelling as a great % of NAV would be cash?

DeleteIts in an 8-k filed subsequent to Q4 results but before the spin. Its small print so to speak in the info statement, but it clearly says that asset sales ahead of the spin will be used to reduce leverage at pre-spin STAR and effectuate the spin.

ReplyDeleteSTHO worth revisiting? Looks like McIntyre initiated as top 5 position and as a very loose rule of thumb for Klarman/Greenblatt spinoffs, looks like we're close to half of the 13mm outstanding shares trading since spin.

ReplyDeletehttps://rb.gy/kt4n9

https://mcvalue.blog/

I keep running through this opportunity but can't pull trigger. Right now my rough thesis is every $11 share of STHO includes basically one SAFE $16 share, and another $6.50 in tangible net assets. So by shorting one share of SAFE for every share of STHO I buy I'd lock in at least $5 of profit. But what holds me back is that STHO is a melting soap bar, I can't see how they end up as anything but a zero. I wouldn't care if they would at least dividend out the SAFE shares directly shareholders but I see no reason they would do it. At their cash burning pace they will need to start selling those shares directly in a couple quarters to fund company liquidation. Anything I'm missing here?

ReplyDeleteI need to catch back up on the story and revisit, I'll revert back in the coming days. Also sort of like the NLOP spin for similar reasons, explicit liquidation mandate, I got a bit burned by ONL, but they were trying to spin an upbeat story. Think NLOP knows better.

Delete