First Horizon Corp (FHN) ($5.3B market capitalization) is a fairly vanilla regional bank serving a balance of both commercial and consumer customers in 12 states throughout the demographically desirable southeastern United States. Unlike other troubled banks, their clientele is less chunky, less hot money, less return motivated. First Horizon doesn't have customer concentration in asset managers, investment funds, tech start-ups or a large wealth management practice where deposits are less operational in nature. It's just a boring middle American bank with a history of above average, low-to-mid teens ROE.

Back in early 2022, First Horizon agreed to be bought out by TD Bank (TD) for $25/share plus a small ticking fee, however on 5/4, the two banks mutually agreed to terminate the merger due to regulatory approval timing uncertainty. It was later reported by the WSJ that the OCC had concerns about TD Bank's anti-money laundering policies and blocked the deal. The merger arb spread had already widened ahead of the termination signaling the market was highly skeptical of this deal going through, but shares tanked anyways as merger arb holders are selling shares at a time when there are few enthusiastic buyers of regional bank shares to match the liquidity. As of this writing, shares trade around $9.60, less than half of where TD was prepared to take it out.

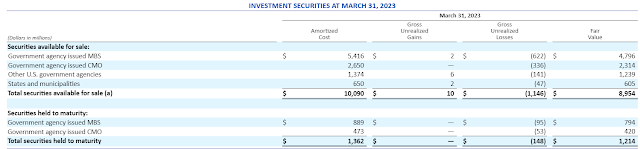

The current banking crisis is different than 2008, there's less concern about the ultimate recoverability of securities on bank balance sheets (AAA CDOs for example, weren't AAA, but there isn't that question with agency MBS), rather the market is more worried about the mark-to-market losses in bank held-to-maturity ("HTM") portfolios if banks are forced to sell securities to meet deposit outflows. First Horizon's use of HTM accounting is relatively small (just 12% of the securities portfolio), deposits (which totaled $61B as of 3/31) large and small would have to flee in mass before the bank would need to realizes losses in their HTM portfolio.

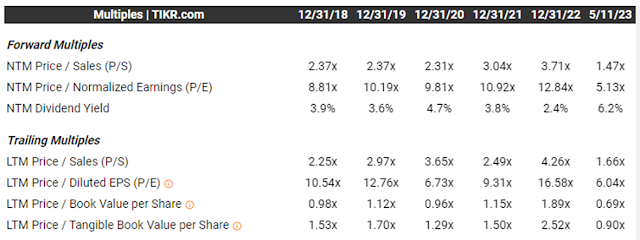

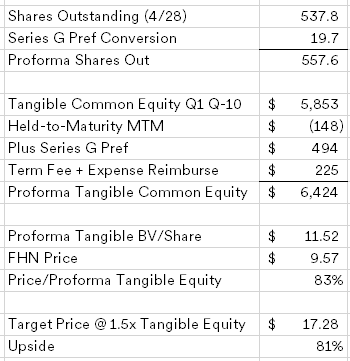

What could FHN be worth once all the clouds clear? Prior to 2022, First Horizon traded around ~1.5x tangible common equity.

- Prior to the termination, some rumors were floating around that TD was looking for a price cut due to market conditions, but First Horizon management stated on their investor call that TD never broached the subject.

- The TD-FHN merger happened due to an unsolicited offer, the bank wasn't running a sale process, so it is unlikely FHN will get scooped up by another bidder in the near term, but also means the board and management take their fiduciary responsibility seriously and would consider other bidders.

- Duration of the investment portfolio is only 5.2 years, each quarter that passes some of the losses will flip as par is realized. The Federal Reserve also appears to be done hiking which should put a floor on the securities portfolio losses.