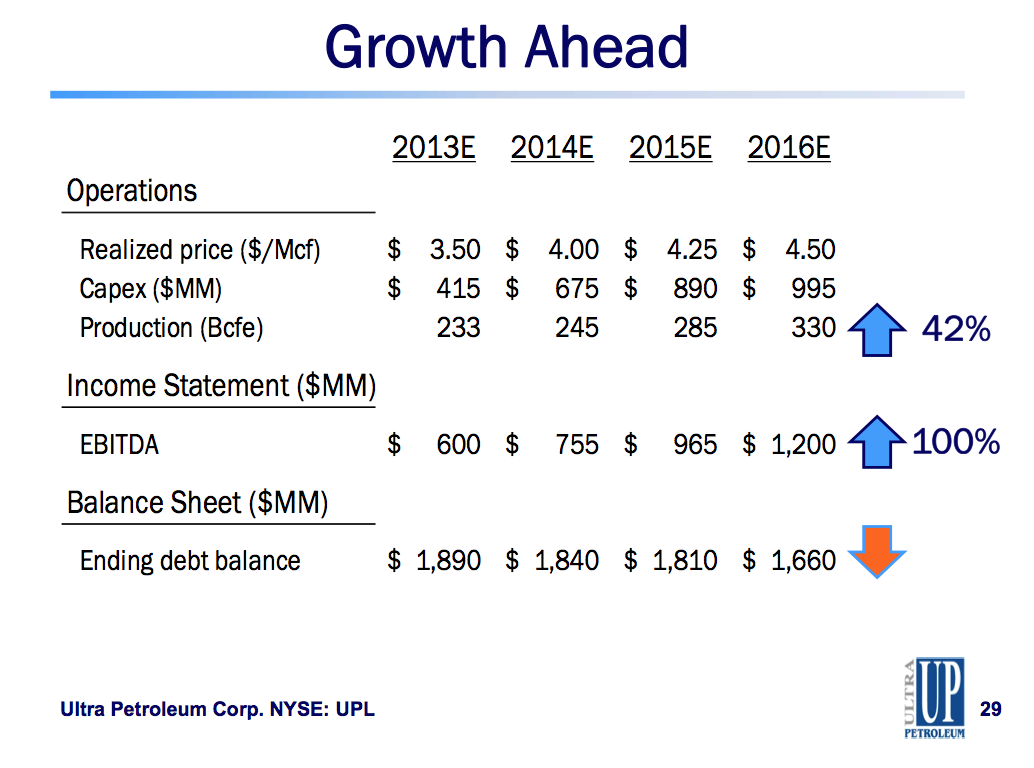

A quick back of the envelope calculation puts the current EV/EBITDA at just under 8 times. Holding that multiple constant and using Ultra's projections for production growth and debt reduction produces the below result as the growth in EBITDA accrues to the equity (170% higher by the end 2016).

Obviously there are a lot of assumptions baked into these numbers, but it shows the opportunity Ultra has to monetize their early life natural gas assets in a normalized pricing environment. If you believe natural gas prices have stabilized, meaning producers show some production restraint now that the market has recovered, Ultra could be a clear winner over the next several years.

Disclosure: I own shares of UPL

No comments:

Post a Comment