Bally's Corporation (BALY) is the old Twin River Worldwide Holdings (old ticker, TRWH) that began with two casinos in Rhode Island, then really starting in 2019 through an aggressive series of complicated acquisitions created a sprawling omni-channel gaming company that appears well positioned to benefit from the long term growth in iCasino and online sports betting. The architect of this transformation is Soo Kim of Standard General, he is the Chairman of the Board and his investment firm owns more than 20% of the shares. On 1/25/22, Standard General submitted a non-binding offer to buy Bally's for $38 per share (shares trade for $35-$36).

The offer appears very opportunistic as the economy is reopening, the pieces of Bally's serial acquisitions are starting to come together but before their true earnings power are fully apparent, all while the market has sold off gaming stocks. Likely Kim is simply highlighting the shares are cheap, he's best positioned to understand the value of the company, and nothing further comes to fruition on the management buyout front. However, now that the acquisition strategy is maturing and the need for a public currency might not be as important, he could actually want to take it private and negotiate a higher price with the board. But at current prices, I agree shares are cheap and would be happy to own the stock absent a deal.

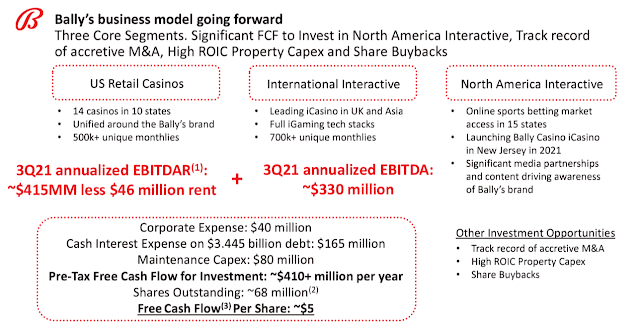

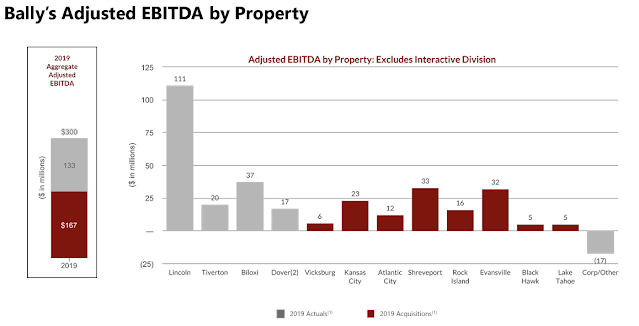

Here's a slide from their investor presentation showing the pace of acquisitions, almost all of the regional casinos were acquired in 2019-2020, many the result of forced divestures when larger gaming peers consolidated. This allowed Bally's to pick properties up on the cheap and build a nationwide footprint in which to standup a mobile gaming presence. I generally prefer the regional casinos to destination ones as they're more stable and proved that throughout covid. Bally's Corp bought the "Bally's" brand name from Caesars (CZR), they're in the process of rebranding all of their regional casinos to the Bally's brand, the old CZR's owned Bally's in Las Vegas (the original MGM Grand) is being rebranded to a Horseshoe property (and Bally's Corp is buying the Tropicana Las Vegas from GLPI).

- On 11/19/20, Bally's entered into an agreement with Sinclair Broadcast Group (SGPI) to rebrand their regional sports networks (the 21 they acquired from FOXA in the DIS deal) from Fox to Bally's, in exchange Sinclair got stock and warrants in Bally's, Bally's also must commit a certain percentage of marketing spend on Sinclair's networks. The cord cutting trend is well known, RSN valuations are down (Sinclair's RSN's debt trade at distressed levels), sports is generally the reason cited for cord cutting because their content is so expensive. But from Bally's angle, this deal puts their brand right in the face of the most engaged sports fans, even if RSNs are losing subscribers, they're unlikely to be losing the ones that Bally's is targeting. While Caesars, MGM or Draft Kings are spending big on the NFL at the national level, Bally's has instead targeted the more engaged local fan, one that might have a more frequent/year-round betting cadence than just the NFL season.

- On 4/13/21, Bally's announced a combination with Gamesys Group (GYS in London) for cash and stock, the deal closed on 10/1/21. Gamesys is a UK based online gaming company (casino strategy versus sports betting, mostly UK and Asian markets) that does both bingo and iCasino games, the idea is to pair the successful Gamesys iCasino offering (where legal in the U.S.) with the Bally's sports betting/Sinclair offering to create an integrated experience. Generally you need a physical presence in a state to get an online license, so in order for Gamesys to fully access the U.S. market they needed to partner with someone like Bally's who thanks to their acquisition spree, have a presence in most of the desirable gaming jurisdictions. To fund the rollout of iCasino and online sports betting in the U.S., both the existing Gamesys international business and the U.S. regional casino business are highly cash generative. Bally's expects to spend 20% of FCF for the next several years on the rollout, but they're taking a more measured pace than other competitors when it comes to promotions, etc.

Why is 9.4x EBITDA cheap?

ReplyDeleteThat's about where regional casinos have traded historically and gives no credit to the iCasino/OSG opportunity in the U.S., plus now it's potentially in play, someone could argue a strategic would have synergies on top of that. They do still own some of their real estate which they could sell for a much higher multiple.

DeleteThank you

ReplyDeleteGamesys stand-alone always traded at <7x EBITDA due to large Japan (grey market exposure)

ReplyDeleteWhat is your opinion of the recent price action with BALY? The price previously returned to the $35-$36 range within a day after the morning selloff in reaction to the Q4 earnings release. So why now is such a large spread opening up between the share price and SG offer price? I have been unable to dig up any news pertinent to the offer or either entity. Does SG have some major exposure to Russian markets which could jeopardize their offer? Or do you think this is simply a result of the broader market activity and is thus a good opportunity to expand the position?

ReplyDeleteProbably just broader market activity, all the gaming names traded down recently, I try not to read too much into these things.

DeleteThe pricing action here both interests & worries me. Are the arbs / speculators heading for the exits or is the general higher interest rate environment & recession talk dampening gaming stocks more generally?

DeleteI'm not following the situation closely so please correct me if I'm wrong but given the potential to fund the vast majority of the transaction through SLBs, wouldn't the only interest rate risk be on the bridge financing?

ReplyDeleteLove your blog.

ReplyDeleteI wonder about these mobile gaming apps. The thing that made casinos so damned profitable the past 70 years was the exclusivity. There was little competition. Vegas, Atlantic City, the horse tracks and state lotteries, keno, &c. Otherwise you were relegated mostly to bingo halls or poker home games.

It's hard to see how the mobile apps become a winner take all situation. If they don't, what prevents competition from turning them all into low margin commodities? Does a gambler care if they place the Steelers bet on Draft Kings, Bet Rivers, FanDuel, BetMGM or any of a dozen others? Or do they care which one is offering the best odds on the spread?

Today we've got one armed bandits in every gas station and truck stop in the Dakotas, tribal casinos blanketing dozens of states, and even fully commercial ventures in major cities like Detroit/Windsor. The American Gaming Association (2020) says there are 987 casinos in 42 states, not including small venues. In that case, the number exceeds 2,000. If I drive 45 minutes in 3 of the 4 cardinal directions, I pass a casino.

On top of this every major casino is competing for mobile sports book and gambling revenues alongside some venture players. On antenna TV when I catch the evening news, bob's burgers, or some bad 90's movie, it's probably close to 1 out of every 5 commercials.

Wampum (Mitchell) is a great book on the history of the tribal gaming industry, if you ever get the itch. I use tribal liberally, as there are truly weak arguments for some of these designations. Mysterious how often these tribal lands happen to be so conveniently located next to large population centers with disposable income and good freeway access.

Thanks for the kind words and good thoughts here. I agree with many of your points but if you also look at the numbers, casinos are well ahead of 2019 numbers, going off of memory, but many of them are up 20-30%, so Americans have a lot of gamble in them.

DeleteAnd don't knock the "one armed bandits in every gas station and truck stop" (I might steal that one), I own ACEL.

I do agree that I doubt if people care that much if they place a sports bet on Draft Kings versus Caesars versus Bally's. Sports betting was historically a low margin business, likely still is, usually is placed in a back corner of the casino for a reason, it is a draw but not the money maker. That's partially why I like BALY's strategy, they're not as aggressive on the sports gambling side, bought Gamesys which is iCasino first, plus they have the physical casinos, I can see an argument for the iCasino being a good marketing tool/funnel for the physical side.

Thanks for the thoughtful comment.

Terminating talks with Standard General, doing a Dutch tender instead.

ReplyDeleteI'll continue to hold -- like the management team, growth opportunities, etc.

Special committee of directors reject the Standard General's bid to take private at $38/sh.

ReplyDelete"Bally’s simultaneously announced that its board of directors determined that Bally’s should pursue initiating a cash tender offer for its shares. It is anticipated that the tender offer will involve $300 million to $500 million, and will be structured in a Dutch auction format. The commencement of the offer is subject to, among other things, obtaining necessary financing and final approval by Bally’s board."

Any take on the dutch auction/rejection?

The tender is potentially pretty big, depending who tenders their shares, could really take out a lot of the free float. Halfway to a public LBO type situation.

DeleteAnd now selected for the Chicago casino. That location is incredible for a casino, on the river, near nightlife, its the old Tribune distribution center for those familiar with the city.

DeleteFrom earnings Call.

ReplyDeletehttps://www.sec.gov/Archives/edgar/data/0001747079/000174707922000069/ex991-excerptedtranscripto.htm

I saw this company as a quick-term trade, but with all debt and the actual interest rate hikes make me feel a bit unconfortable.

Im wondering how much will increase margins in the mid term.

PD: Sorry for my english.

I said in the post that I'm content owning the business if the buyout offer didn't go through, meant that, think it has some upside as all the pieces come together. If it was just a quick trade for you, the company will be doing a tender offer, probably lets most of the speculation arbitrage buyers out at a decent price.

DeleteMDC, any comment about risk of interest rate on the company? Making such a huge tender offer with all-ready leverage balance sheet seems wired. any thought about how you look at this?

ReplyDeleteIt kind of depends on your view of how high rates are going to go? I probably land on the side that inflation will retreat sooner than later given all the destruction of capital and demand happening. Bally's current term loan is LIBOR + 325. They also have a lot of embedded real estate value and committed partner in GLPI. I'm not particularly worried, do find the situation quite interesting now that they could really shrink the float substantially if insiders don't tender, this would be a public LBO essentially.

Deletehttps://investors.ballys.com/news/news-details/2022/Ballys-Commences-Modified-Dutch-Auction-Tender-Offer-To-Purchase-Up-To-190-Million-Of-Its-Outstanding-Common-Shares/default.aspx

ReplyDeleteInteresting little buyback scheme! I like it. Will you be placing an offer? What do you think about it?

Probably not, but I need to think about it more in relation to my other ideas.

DeleteMore interestingly, they posted an 8-K with their 3 year cash flow plans including the Chicago build out:

https://www.sec.gov/Archives/edgar/data/1747079/000110465922074117/tm2219368d1_ex99-1.htm

Im having dejavu with this name

ReplyDeleteSame, kicking it around a bit, but not sure I'll fall for the fake bid twice.

Delete