- Ladder is an internally managed REIT with significant insider ownership and management seems to run the company as owners versus as a fee revenue stream.

- Senior secured portfolio -- in particular their CMBS portfolio is predominantly AAA (which the Fed recently announced is eligible for TALF financing) versus many of their peers who play in the BBB to B space and have had trouble with margin calls.

- Unsecured and term repurchase financing gives Ladder the opportunity to work with their borrowers on modifications without getting cash flows shut off like they would in a CRE CLO or face margin calls as they would in short term repo.

Quick overview of Ladder Capital, they were founded shortly following the last market crisis in 2009 (and listed in 2014) by the former UBS real estate team, that team is still largely together today and as a group own 11% of the company. Ladder primarily plays in four areas of CRE finance: 1) transitional whole loans held for investment; 2) stabilized whole loans to be sold into CMBS (hopefully recognizing a gain on sale); 3) CMBS held for investment; 4) single tenant net lease properties; and then they do have a small sleeve of other operational properties partially the result of any foreclosures on the whole loan portfolio. They portray themselves as having a strong credit culture and that seems to have played out in the last several years, prior to the coronavirus crisis, they've only had one realized loss on a loan, and unlike other mortgage REITs they don't have any legacy issues or at least don't play the trick of segmenting a core and legacy portfolio when things don't go as planned.

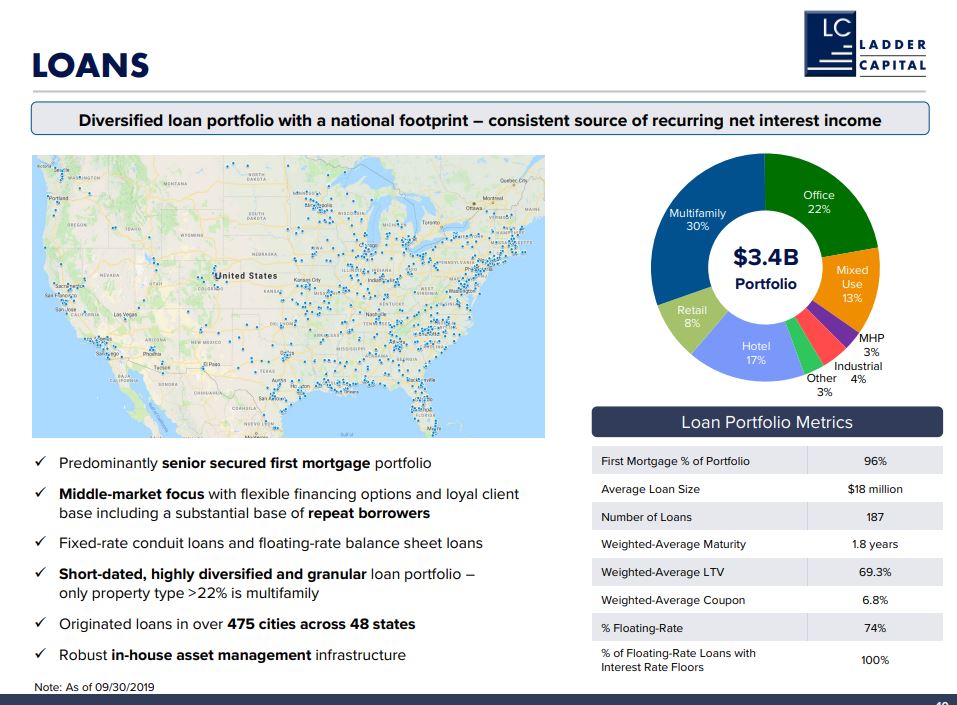

Roughly half of their assets fall into the first and second category, commercial real estate loans that Ladder originates themselves either on transitional properties (meaning a developer is re-positioning the property in some way) for their own balance sheet or on stabilized properties which Ladder will originate to distribute via the CMBS market. Many if not most of the transitional variety will require some kind of forbearance or modification, construction crews may or might not be working, and certainly any up leasing activity or the time to rent stabilization where the property could be refinanced with longer term financing is pushed out. The CMBS conduit market is already showing early signs of thawing, and on their Q4 call, Ladder mentioned having a fairly small amount of loans "trapped" in their warehouse awaiting to be sold into the CMBS market. Here's their slide on their loan portfolio as of January:

As you can see, about 25% of the portfolio is exposed to the highest risk retail and hospitality sectors. Given their middle market lean, the hospitality portfolio tends to be more weighted towards self service than convention hotels or resort destinations that may take longer to recover. I tend to think most of these mortgage REITs have similar assets, capital is a bit of a commodity, but possibly Ladder is more conservative than some others.

As you can see, about 25% of the portfolio is exposed to the highest risk retail and hospitality sectors. Given their middle market lean, the hospitality portfolio tends to be more weighted towards self service than convention hotels or resort destinations that may take longer to recover. I tend to think most of these mortgage REITs have similar assets, capital is a bit of a commodity, but possibly Ladder is more conservative than some others.

The right side of the balance sheet is where I think Ladder is more interesting than others -- many commercial mREITs finance their transitional loan portfolios through CRE collateralized loan obligations ("CRE CLOs") where the loans are pledged to an off balance sheet SPV which then issues notes to fund the SPV's purchase of the loans. The notes will be issued in various tranches depending on investor risk tolerance with the sponsor (the mREIT) of the CLO retaining the junior bonds and equity. If the underlying collateral doesn't perform, there are asset coverage tests in place to divert cash flows from the junior note holders to pay the senior note holders and protect their position in the transaction. In the years following the financial crisis, the asset coverage test thresholds are paper thin to the point where one or two modified loans in the portfolio will trip the diversion of cash flows away from the mREIT to pay down the senior note holders. In practice, what often happens is if one of the underlying loans is in default or requires modification, the mREIT will purchase the loan from the CLO at face value and work it out off to the side as to not jeopardize their cash flow lower down the payment waterfall. However, in the current environment where there will be many defaulted or modified loans, it might be difficult or just not possible due to margin calls elsewhere in an mREIT's balance sheet to purchase the non-performing loans from the CLO and thus shutting off cash flows.

Ladder had previously issued two CRE CLOs but wound those vehicles up in October and is currently out of that market. Instead, Ladders funds its loans through a combination of unsecured bonds where they are a BB credit and through term repurchase facilities. In their term repurchase facilities, they've always stressed in their filings that they've always kept a cushion available to allow them to meet margin calls in a cashless manner. Neither have the feature of a CLO where cash flow of the underlying assets is completely shut off and may allow Ladder some breathing room in working through modifications with borrowers. Here's from p74 of the 10-K, they've received margin calls and met them thus far (at least what's been disclosed), many mREITs tout their total available credit capacity but I think that's less meaningful than the borrowing capacity on their currently pledged assets.

Since I started drafting this post, Ladder put out an additional "business update" press release that is becoming all to regular for public companies these days. In it they outline how they have $600MM of cash after some maturities on their loan portfolio plus they sold assets at 96 cents on the dollar and they have $2.3B of unencumbered assets. Should be sufficient to get them through the crisis? The dividend is roughly 20% at $1.34/year, that'll almost certainly get cut/suspended and could provide an attractive opportunity if any remaining yield pigs remain holders. I like the management here and think we will see most if not all CRE CLOs fail their coverage tests (might be more opportunities once that happens), my sense is Ladder should trade for somewhere in the 75-80% of 12/31 book value range, no science behind it, but I see little risk that they'll be forced to liquidate at fire sale prices or have their cash flows shut off due to asset coverage test failures.

Roughly half of their assets fall into the first and second category, commercial real estate loans that Ladder originates themselves either on transitional properties (meaning a developer is re-positioning the property in some way) for their own balance sheet or on stabilized properties which Ladder will originate to distribute via the CMBS market. Many if not most of the transitional variety will require some kind of forbearance or modification, construction crews may or might not be working, and certainly any up leasing activity or the time to rent stabilization where the property could be refinanced with longer term financing is pushed out. The CMBS conduit market is already showing early signs of thawing, and on their Q4 call, Ladder mentioned having a fairly small amount of loans "trapped" in their warehouse awaiting to be sold into the CMBS market. Here's their slide on their loan portfolio as of January:

The right side of the balance sheet is where I think Ladder is more interesting than others -- many commercial mREITs finance their transitional loan portfolios through CRE collateralized loan obligations ("CRE CLOs") where the loans are pledged to an off balance sheet SPV which then issues notes to fund the SPV's purchase of the loans. The notes will be issued in various tranches depending on investor risk tolerance with the sponsor (the mREIT) of the CLO retaining the junior bonds and equity. If the underlying collateral doesn't perform, there are asset coverage tests in place to divert cash flows from the junior note holders to pay the senior note holders and protect their position in the transaction. In the years following the financial crisis, the asset coverage test thresholds are paper thin to the point where one or two modified loans in the portfolio will trip the diversion of cash flows away from the mREIT to pay down the senior note holders. In practice, what often happens is if one of the underlying loans is in default or requires modification, the mREIT will purchase the loan from the CLO at face value and work it out off to the side as to not jeopardize their cash flow lower down the payment waterfall. However, in the current environment where there will be many defaulted or modified loans, it might be difficult or just not possible due to margin calls elsewhere in an mREIT's balance sheet to purchase the non-performing loans from the CLO and thus shutting off cash flows.

Ladder had previously issued two CRE CLOs but wound those vehicles up in October and is currently out of that market. Instead, Ladders funds its loans through a combination of unsecured bonds where they are a BB credit and through term repurchase facilities. In their term repurchase facilities, they've always stressed in their filings that they've always kept a cushion available to allow them to meet margin calls in a cashless manner. Neither have the feature of a CLO where cash flow of the underlying assets is completely shut off and may allow Ladder some breathing room in working through modifications with borrowers. Here's from p74 of the 10-K, they've received margin calls and met them thus far (at least what's been disclosed), many mREITs tout their total available credit capacity but I think that's less meaningful than the borrowing capacity on their currently pledged assets.

The other issue many mREITs are having is with their CMBS portfolios, mREITs like XAN or CLNC tend to buy CMBS in the BBB-B rating range or simply unrated, Ladder is predominately in the AAA and AA rated tranches of CMBS and as a result have significant credit enhancement via subordination. While the pricing of AAA CMBS did drop, the Fed recently announced an expansion of the TALF program in which they'll provide financing on AAA CMBS issued prior to 3/23/2020. In a bit of a departure from the other assets classes they're willing to finance, CMBS will only be legacy versus only new issuance. I take this two different ways, 1) the Fed wants to stabilize CMBS prices today; 2) they're not concerned with needing to provide support for new issuance to resume like they are in other ABS markets. Both are good for Ladder as a CMBS investor and as a loan originator to the CMBS market and it seems to be having its intended result, take the iShares CMBS ETF for example (tracks investment grade CMBS), it has recovered its losses and is up on the year.Committed Loan FacilitiesWe are parties to multiple committed loan repurchase agreement facilities, totaling $1.8 billion of credit capacity. As of December 31, 2019, the Company had $702.3 million of borrowings outstanding, with an additional $1.0 billion of committed financing available. Assets pledged as collateral under these facilities are generally limited to first mortgage whole mortgage loans, mezzanine loans and certain interests in such first mortgage and mezzanine loans. Our repurchase facilities include covenants covering net worth requirements, minimum liquidity levels, and maximum debt/equity ratios.We have the option to extend some of our existing facilities subject to a number of customary conditions. The lenders have sole discretion with respect to the inclusion of collateral in these facilities, to determine the market value of the collateral on a daily basis, and, if the estimated market value of the included collateral declines, the lenders have the right to require additional collateral or a full and/or partial repayment of the facilities (margin call), sufficient to rebalance the facilities. Typically, the lender establishes a maximum percentage of the collateral asset’s market value that can be borrowed. We often borrow at a lower percentage of the collateral asset’s value than the maximum leaving us with excess borrowing capacity that can be drawn upon at a later date and/or applied against future margin calls so that they can be satisfied on a cashless basis.Committed Securities Repurchase FacilityWe are a party to a term master repurchase agreement with a major U.S. banking institution for CMBS, totaling $400.0 million of credit capacity. As we do in the case of borrowings under committed loan facilities, we often borrow at a lower percentage of the collateral asset’s value than the maximum leaving us with excess borrowing capacity that can be drawn upon a later date and/or applied against future margin calls so that they can be satisfied on a cashless basis. As of December 31, 2019, the Company had $42.8 million borrowings outstanding, with an additional $357.2 million of committed financing available.Uncommitted Securities Repurchase FacilitiesWe are party to multiple master repurchase agreements with several counterparties to finance our investments in CMBS and U.S. Agency Securities. The securities that served as collateral for these borrowings are highly liquid and marketable assets that are typically of relatively short duration. As we do in the case of other secured borrowings, we often borrow at a lower percentage of the collateral asset’s value than the maximum leaving us with excess borrowing capacity that can be drawn upon a later date and/or applied against future margin calls so that they can be satisfied on a cashless basis.

Since I started drafting this post, Ladder put out an additional "business update" press release that is becoming all to regular for public companies these days. In it they outline how they have $600MM of cash after some maturities on their loan portfolio plus they sold assets at 96 cents on the dollar and they have $2.3B of unencumbered assets. Should be sufficient to get them through the crisis? The dividend is roughly 20% at $1.34/year, that'll almost certainly get cut/suspended and could provide an attractive opportunity if any remaining yield pigs remain holders. I like the management here and think we will see most if not all CRE CLOs fail their coverage tests (might be more opportunities once that happens), my sense is Ladder should trade for somewhere in the 75-80% of 12/31 book value range, no science behind it, but I see little risk that they'll be forced to liquidate at fire sale prices or have their cash flows shut off due to asset coverage test failures.

Disclosure: I own shares of LADR