This is a similar idea to WMC, Acres Commercial Realty (ACR) ($73MM market cap) is also a mortgage REIT trading at a similar discount to book value (38% of BV) but without the near term catalyst of a potential sale. ACR has gone through a few name and manager changes over the years, it was originally Resource Capital (RSO), then became Xantas Capital (XAN), and following a 2020 margin call of their CMBS portfolio, current management came in and once again rebranded. This is my third bite at the apple and is less of a short term event driven idea and more a 2-3 year transformation path back to a normal commercial mREIT.

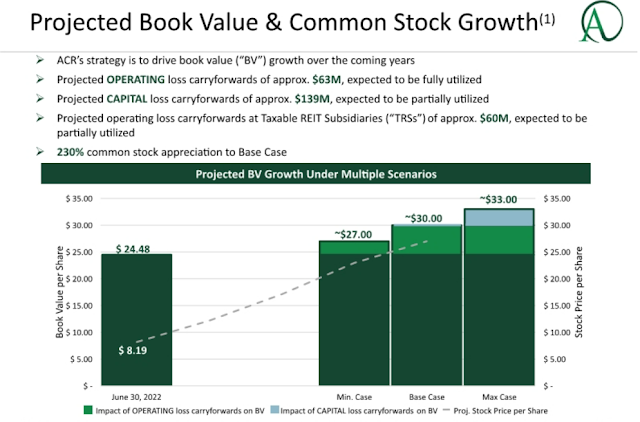

While ACR doesn't have the near term catalyst of WMC, the assets and balance sheet are cleaner at ACR and a majority of the cheap price can be attributed to its small size, current market conditions and lack of a dividend, the latter being the main appeal of mREITs to retail investors. The reason ACR doesn't pay a dividend is two fold, both of which should appeal to readers of this blog: 1) since shares trade at a significant discount, management have been buying back shares, approximately $30MM worth (significant for an entity this size) since November 2020, with $10MM remaining on their authorization; 2) following the 2020 margin call, ACR has a significant amount of both net capital losses and net operating losses ("NOLs"). To monetize the net capital losses, ACR has created a side pocket of opportunistic equity real estate investments with turnaround plans that if executed should generate taxable income or gains. Those proceeds would then be reinvested in the core business of originating and holding transitional commercial real estate loans. The tax asset is valued at $21.6MM (again, meaningful for an entity this size), but has a full valuation allowance against it on the balance sheet. Once the tax assets are soaked up and the shares trade closer to book value, the REIT will turn the dividend back on and retail investors should return.

ACR lays out the tax monetization strategy in one of their slides, but this doesn't include the potential for more accretive buybacks. Shares currently trade for $9.26 vs. $8.19 below and I wouldn't count on it trading for book ($24.48) anytime soon, but the math they layout is quite attractive.

ACR's core business is originating and holding "transitional" commercial real estate loans, this typically means ACR will help a developer or investor finance a value-add property, the equity owner will execute on their plan over a couple year period and then will refinance the property at stabilization, taking out ACR's loan in the process. Over 3/4ths of ACR's loans are to multi-family properties, I remain reasonably bullish on this sector, at least from a lender's perspective. With interest rates increasing, potential new homeowners will be stuck renting for a few more years and ACR's heavy concentration to FL and TX (44% between the two) should have continued demographic tailwinds as people/businesses migrate to sunny skies and lower cost of living geographies. If multi-family properties do get hit, ACR does have a reasonable equity cushion below each loan with a weighted average loan-to-value of 72%. ACR's loans are floating rate, thus should have minimal duration risk, although as rates continue to increase, that added interest expense borne by their borrowers will start to increase credit risk at a certain point.

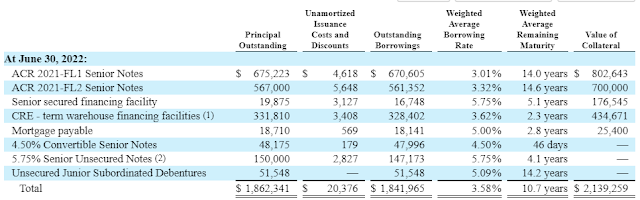

To fund their loans, ACR predominately relies on the CRE CLO market.

Newly originated loans are placed in the "CRE - term warehouse financing facilities" and once of sufficient size, they'll raise longer term CRE CLO financing (also floating rate) and transfer the warehoused loans into the CRE CLO. ACR retains the junior bonds and equity of the CLO. CLOs are great because they're not mark-to-market vehicles and give the manager flexibility to repurchase problem loans inside the SPV to avoid any tests failing that would cause cash flows to be diverted from junior tranches. During the height of covid, CRE CLOs continued paying all noteholders and no test failures occurred, unlike in the CMBS market where the collateral has an observable mark and was financed via repurchase agreements that were marked-to-market daily. The CRE loans inside ACR's CLOs are whole loans that are not syndicated and don't have live marks available on them. ACR is likely still being punished for 2020, but the manager is gone and the CMBS assets that cause the blow up are gone too. The CLOs originated by the old manager all performed fine.

There is an external manager here, Acres Capital, with a fairly traditional mREIT fee agreement that includes a base fee of 1.5% of equity and 20% of earnings above a 7% hurdle, that's not great, but they otherwise seem to be doing the right thing even if it goes against their incentive in the near term (like buying back a significant amount of stock). One thing I don't like about the fee agreement, the manager receives 25% of their incentive fee paid in stock, at this discount that's highly dilutive to minority shareholders. But overall, they own 6+% of the company and seem to be reasonable corporate stewards. There is also the presence of two sophisticated credit investors which is a plus, Oaktree remains a significant shareholder following the 2020 bailout with 9% and First Eagle Credit Management (large CLO equity investor, they manage ECC which owns CLO equity and bonds) with 12.5% of common, plus a good slug of the preferred stock (check those out if you like yield).

Most of the commercial mREITs are trading at a discount to book value in today's market, the best of breed like Starwood Property Trust (STWD) and Arbor Realty (ABR) trade right at book, but even the small cap external peers like NexPoint Real Estate Finance (NREF) and Lument Finance Trust (LFT) trade for about 2/3rds of book (both pay a low double digit dividend), putting the same multiple on ACR would be about 75% upside.

Disclosure: I own shares of ACR