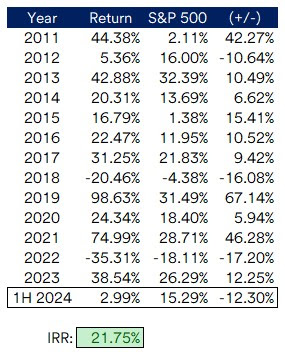

Welp, it was bound to happen, but I underperformed the broad U.S. market by an embarrassing amount this year. My portfolio lost -6.39% compared to the S&P 500's 25.02% gain in 2024, however my lifetime-to-date IRR is still hanging in just above 20%.

I spent the last couple weeks going back through my portfolio, reaffirming the thesis for each, below are the elevator style pitches for my current holdings (didn't have enough time to discuss closed positions, if you have any questions on those, feel free to comment):

Rumored M&A:

Coincidentally, these are all land bank companies where the strategic review processes are getting a little long in the tooth, creating varying levels of anxiety in each situation.

- CKX Lands (CKX) is an illiquid microcap that owns land in Louisiana that it primarily monetizes via oil and gas royalties. About 500 days ago, the company announced a review of strategic alternatives and this past spring updated CKX had received interest from multiple parties, but that was close to 9 months ago now. A commenter posted on 12/4, an email from Gray Stream (Chairman & President, who is working on an expired contract) confirming that CKX Lands is not involved in the Project Cypress sequestration effort, but also that strategic alternatives "efforts and discussions are still ongoing in earnest. We hope to have a material update soon." I do worry that a no deal announcement will significantly hurt the stock, it trades very little on a daily basis, is semi-popular in small cap value circles and a no-deal would signal a dead money stock for years to come. If it doesn't get sold after this long process, when will it? Let's hope something is in the works and announced soon. My best guess is still something gets done, but my expectations are for a lower premium, something in the $15-17/share range.

- Howard Hughes Holdings (HHH) is now a pure-play master planned community real estate developer following the spinoff of Seaport Entertainment Group (SEG). A week after the spinoff, Bill Ackman's Pershing Square Holdings (37.5% owner) updated their 13D to state their interest in taking the company private. It's five months later, we don't have much of an update, Bill is busy discussing politics and his investments in Fannie and Freddie on Twitter, which is a bit concerning. I thought something would be done by now (had some December call options that unfortunately expired worthless, still have a few January calls that are out of money), there's not going to be another bidder for the company that can pay a full price, management would be best to take a fair deal from Pershing Square versus continuing to trade at a discount into eternity. My current best guess, they come to a deal for $90-95/share sometime in January.

- Limoneira (LMNR) is a lemon grower and packager that is increasingly moving acreage to avocados, but that will be a several year transition. Limoneira also has a real estate development arm which has a JV developing homesites from their former agricultural land. 13 months ago, the company announced they were pursuing strategic alternatives, we haven't seen too much of an update, other than mentions of "significant interest". In August, the company added a new incentive agreement with senior management to provide bonuses for a transaction over $28/share ("Base Share Price") with escalators up to $40/share ("Target Share Price"), and then even greater escalators above that. Shares trade today below $25/share after the stock dipped a bit following 2025 guidance disappointed a bit, but the long term story seems in place. I'm still anticipating a deal above $28/share, my only concerns is it could be a complicated deal (resulting in an attractive headline premium, but the market valuing it at a discount), management has mentioned exploring OpCo/PropCo structures as part of this process.

Spinoffs:

- Enhabit Inc (EHAB) is a mid-2022 spinoff of Encompass Health (EHC), like many spins, Enhabit was spun with too much debt and a management team that didn't appear ready for life as a public company. They stumbled right out of the gate and attracted activist investors who pushed for a sale. No sale appears on the horizon near term (insurers like UHC were previously buyers, but they're tangled up in other issues right now), but at ~8.5x EBITDA (when similar comps have been sold for mid-teens multiples or higher) it seems relatively cheap. The home health and hospice sector should have similar tailwinds to senior housing with the aging population, but home health has the added benefit of being more cost effective and keeping seniors in their homes. Enhabit has a lot of leverage, 4.8x EBITDA, would like to see that come down to more tolerable levels for public markets, this isn't my highest conviction idea, but does seem like a reasonable setup to outperform from the initial spin disappointment.

- Inhibrx Biosciences (INBX) is the spinoff of Inhibrx Inc, basically a restart of the development engine after selling INBRX-101 to Sanofi. New INBX has two ongoing trials, the further along one, a registration-enabling phase trial for INBXR-109 should have a data readout in mid-2025. I'm just along for the ride, no thoughts on the pipeline, just letting the spin play out over 1-2 years post Sanofi transaction.

- Seaport Entertainment Group (SEG) is the Howard Hughes spin, they did complete their rights offering and now we look forward to their first earnings call in March which will be their management's first chance to tell their story to the market. There's a lot of wood to chop here, yes, SEG owns a full Manhattan block, but its extremely underutilized (seen plenty of pictures on Twitter of it near empty). I do like the management team that was brought in to run SEG, but also cautious on the speed of change, my best guess is a mixed use tower at 250 Water in the Seaport District is the first development project undertaken. With two mega resorts opening this year and a new casino/stadium complex being constructed at the former Las Vegas Tropicana site, assigning any value to the Fashion Show air rights seems a ways away.

Broken Biotech Basket:

- On 11/8/24, AlloVir (ALVR) announced a reverse merger agreement with privately held Kalaris Therapeutics, this proposed merger includes no oversubscribed PIPE, special dividend or CVR to current AlloVir shareholders which are features of deals that have recently gotten a post announcement pop. Instead, AlloVir will be bring essentially all of the proforma cash ($100MM) to closing and receive 25% of the company, putting a fairly lofty valuation on Kalaris, which only just commenced enrollment in a Phase 1 trial. $100MM cash on 115.5 million ALVR shares is roughly $0.86/share, despite that, shares currently trade for $0.42/share. ALVR shareholders owning 29.4% have already pledged their support for the merger, the deal is expected to close in Q1, voting this one down might be difficult, but it seems too cheap to sell now. There might be some tax loss selling happening and once the deal closes, maybe we get some uplift from continued shareholder rotation as the story gets out. But now very low conviction.

- On 10/31/24, Aerovate Therapeutics (AVTE) announced a reverse merger agreement with privately held Jade Biosciences, unlike AlloVir, this merger includes a special dividend of virtually all of AVTE's remaining cash at close (estimated at $65MM or $2.25/share, but that might be conservative) and a large $300MM oversubscribed PIPE. Post closing, AVTE shareholders will only own 1.6% of the combined company. This is a liquidation that's structured as a reverse merger, the best kind of outcome. The plan is to hold through the special dividend / merger and then exit shortly after as those that didn't get their full allocation in the PIPE might bid up the shares.

- ESSA Pharma (EPIX) recently announced the termination of their License Agreement, further solidifying their pursuit of a liquidation or reverse merger. Other than that, nothing has really changed since my write-up in early November, the spread between my estimated liquidation value of ~$2.15/share is about 20% above where the $1.79/share it trades today. Tang Capital and BML Capital are both just under 10% holders here, the cash pile here is a healthy $100+MM, this is probably my current favorite in the basket.

- Ikena Oncology (IKNA) snuck in a reverse merger transaction before year end, announcing on 12/23 a deal with Inmagene Biopharmaceuticals that includes a CVR plus an oversubscribed $75MM PIPE from both current IKNA investors and new names. This reverse merger hasn't been well received by the market, I'm a bit surprised by that given the PIPE, but there will be limited return of capital here (maybe a token special dividend if the cash at close is above $100MM) compared to AVTE. The PIPE values IKNA at approximately $120MM or $2.40+/share, despite that, shares currently trade at $1.64/share. The deal is targeted to close in mid-2025, I would anticipate the price will rally a bit from here into the close as the shareholder registry turns over.

- Nothing has really changed at Athira Pharma (ATHA) since my early November write-up, shares are down mid-single digits since, it might be a bit more attractive now as we wait for a potential deal with 14% holder Perceptive Advisors. This one is a little more risky, rather than waiving the white flag following a failed clinical trial, Athira has stated they're doubling down on their development pipeline. Shares trade at $0.59/share, a wide discount to my estimated liquidation value of $0.86/share.

- HilleVax (HLVX) reported a failed clinical trial in July along with a vague intention to "explore the potential for continued development" of their pre-clinical assets, but on 12/5, we received further validation this situation is a regular-way broken biotech seeking strategic alternatives with the announcement HLVX was doing a 70% reduction in force, including three executive officers. There's still work to do before this is a clean shell, cash burn is higher than I expected as R&D expenses didn't come down much in Q3 despite halting the trial in early July, HLVX also still has yet to terminate their significant operating lease. Shares still trade at a discount to my updated liquidation value of approximately ~$2.50/share.

REITs:

- ACRES Commercial Realty Corp's (ACR) share price performed surprisingly well (+60%) this year despite the slow motion train wreck that is commercial real estate. ACR had a few foreclosures this year, but mostly sidestepped the worst of it, although 23% of their loan portfolio is rated 4 or 5, the quality loans can refinance out of their bridge loans but the junk can't. This commercial mREIT is essentially in runoff at the moment, they haven't had much if any new origination this year and their CRE CLOs are outside of the reinvestment period. They do have a handful of owned real estate positions where they've guided to monetizing at a profit over the next several quarters in order to soak up their tax assets. Once the tax assets are exhausted, the plan is to turn the dividend back on, hopefully re-rate from ~$16/share somewhere closer to ~80% of the $27.92/share book value. That's possibly a 2025 story.

- Creative Media & Community Trust Corp (CMCT) is a total dumpster fire caught up in a death spiral of preferred redemptions into common stock that then get puked out, which encourages others to puke it for the tax loss. On the positive side, CMCT was able to refinance their hotel property which is one of the several assets they plan to put asset level debt on to repay their non-compliant credit facility. We'll see if tax loss season ending will cause the stock to recover, from the action on 12/31, that might be the case, but a bit too early to tell. My current plan is to own this a little longer than just for a January effect bounce, think the real juice could be if they are able to stabilize and show progress in the strategic shift to multi-family.

- Enzo Biochem Inc (ENZ) is a two-step liquidation, after selling their clinical lab division to Labcorp in mid-2023, they're left with a subscale unprofitable life sciences division. The market seems to be losing in faith that ENZ will actually be able to monetize their remaining division and return cash to shareholders, in mid-December, ENZ released their fiscal Q1 results disclosing a 20% revenue decline due to "general continued headwinds in the life sciences tools space" without much other detail on the ongoing strategic process, which wasn't confidence inspiring. On the positive side, ENZ did appoint Jon Couchman to the Board, he has previous liquidation experience. Following my experience with PSFW, a similar two-step liquidation that took a long time to fully play out, I'm willing to give this one some space too.

- HomeStreet (HMST) is a zombie bank, their balance sheet is upside down as a result of the Fed taking rates up to combat inflation. HomeStreet had a deal with FirstSun Capital Bancorp (FSUN) to be sold in a stock-for-stock deal that valued HMST at approximately $15/share, but regulators balked at the deal, especially as FSUN forum shopped their regulatory/charter structure from the OCC to a Texas state charter. The primary concern of Texas regulators was HMST's commercial real estate exposure (they have a significant slug of Class B/C multifamily loans in the LA area, regulators have been spooked on that market since NYCB had their struggles this past spring). The FirstSun deal broke, HMST has responded by selling $990MM of their commercial real estate portfolio (about 20% of the CRE exposure) to Bank of America for 92 cents on the dollar, which is 4 cents lower than where they've marked the fair value of their overall loans held for investment on their balance sheet. The longer HMST stays standalone, the worse, hopefully they get pushed into the arms of a new merger dance partner here soon at a similar ~$15/share valuation. Many are predicting 2025 as the year of regional bank mergers, hopefully HMST is one of the first taken out.

Legacy Positions:

- While significant holdings for me, Green Brick Partners (GRBK), Mereo BioPharma Group PLC (MREO) and to a lesser extent Par Pacific Holdings (PARR), these legacy positions are not really active actionable ideas in my mind. Happy to chat with others fellow investors, but for now I'm just letting these investments play out and defer capital gains taxes.

Performance Attribution:

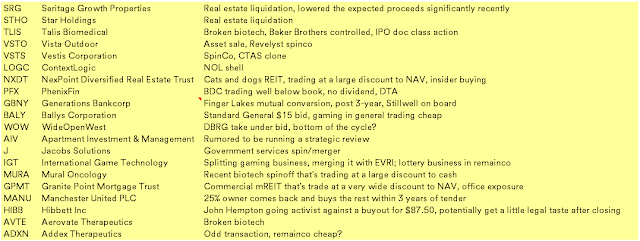

Current Watchlist:

As always, interested in hearing new ideas, please post in the comments, in the spirit of sharing, here's my current watchlist with a few notes on each. The blue are the busted up biotechs that I've been looking at, but didn't make it into the portfolio yet for one reason or another.

Current Portfolio:

Disclosure: Table above is my taxable account, I don't manage outside money and this is only a portion of my overall assets. As a result, the use of margin debt, options or concentration does not fully represent my risk tolerance.