This will be a relatively quick one, thank you to Writser for pointing me in this direction.

Magenta Therapeutics (MGTA) (~$47MM market cap) is another addition to my growing basket of failed biotechnology companies that are pursuing strategic alternatives like a reverse merger or liquidation. Magenta is a clinical stage biotech focused on improving stem cell transplantation. Their primary product, MGTA-117, initially had positive data readouts in December for their ongoing Phase 1/2 trial, but shortly after, patients using higher doses started experiencing adverse effects, culminating with the death of one trial participant and the subsequent shutdown of the MGTA-117 clinical trial. Then yesterday afternoon, Magenta announced they were going to explore strategic alternatives, the press release is rather vague and generic. But similar to SESN and others, I anticipate Magenta first trying to explore a buzzy reverse merger with a more promising biotech, if that doesn't work, pursue a liquidation.

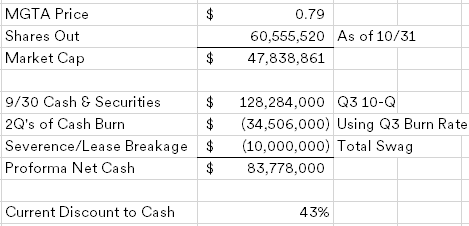

Magenta's balance sheet is fairly simple, they had $128.3MM in cash and treasuries as of 9/30, no debt other than subleased space in a Cambridge, MA office/lab complex.

Since we're getting close to half way through Q1, I annualized the Q3 burn rate for two quarters. The company hasn't given any initial indication of eliminating their workforce (as of the last 10-K, they had 75 people), but I expect that to follow shortly, along with breaking their lease. Cambridge is a biotech hot spot, Magenta or the primary lessee shouldn't have too much trouble finding a new tenant. Feel free to make your own assumptions, but I come up with MGTA trading at about a 40% discount to proforma net cash even after spiking on the news today. In terms of other assets, Magenta does have $247.2MM in NOLs and two other early stage product candidates (one has a Phase 2 trial ongoing), but as always, difficult to put a value on those.

The primary risk here could be the company deciding to double down on their two other early stage products, but the discount is wide enough here to warrant an add to the basket.

Disclosure: I own shares of MGTA

Hi, thanks for this.

ReplyDeleteWhat are the other Biotechs in your portfolio please?

I usually have 1-2 of these, they come and go out of the portfolio. Currently: MGTA, MREO, SESN, and SIOX. But have many others on my watchlist: ABIO, CMRX, MACK, OTIC, STSA, NBRV, FNCH and MTCR.

DeleteI also like OTIC very much especially after the recent announced assets sale, which should add about $0.07 per share. Interesting that price hasn't moved much after that.

DeleteI'm probably stupid but I don't understand why you would like OTIC. $41m cash, $5m in accrued expenses, debt costs $17m, lease costs $4m+, severance charges $5m. Prevail deal net adds back $5m or something like that for a total of ~$15m or $0.26 per diluted share. But last quarter they burned $12m. Even if you assume burn comes down significantly, at $4m for two quarters (which I think is optimistic) there's already not too much upside left.

DeleteAm I making a mistake somewhere?

Right burn based on assumptions relating to employee severance, which began in August with initial $1.5M charge when they cut by 55%, $5M Q4 charge with removing the rest of the workforce. My understanding is that the only employee left is the former CFO working on an hourly basis. My liquidation numbers on the upside are max $0.22 per share..

DeleteThe estimates are similar. Difference could be in prepaid assets in this case could make big difference. My max liquidation estimate is $0.18/share.

Delete-$4.4M for lease termination -$5M for employee termination -$25.25M for liabilities + $43.9M net current + $5M for OTO 825 -$1.15M for OTO 825 payment +$0.25M OTO 413 + $0.156M OTO 413 patents - $1M for contingency reserve = net cash 12.476M / 57.153M shares outstanding = 0.218 per share

DeleteI'm assuming severance = total comp for the quarter which may be wrong

DeleteIf they paid the 45% remaining employees with full expenses for research and SG&A (which is unlikely) I get an additional -$5.4M and net cash per share in liquidation at $0.124 per share

Deletefwiw this is my first time following a company with a position into a non-bankruptcy liquidation with proceeds to equity holders

Deletere: OTIC, the correct share count is closer to 68 - 69mm shares. There are pre-funded warrants that were issued last year that need to be added to the shares outstanding.

DeleteYep, the share count is off. Also, $5m costs from September until February is _absolutely_ way too optimistic. Apart from the severance payments they had to pay salaries until mid-December, legal & consultancy costs, costs to prepare the proxy and hold a meeting, probably some legacy R&D costs, rent (they did not manage to sublease their facility), etc. Also, you cannot just net prepaid assets against accrued costs because the prepaid assets include stuff that is worthless in a liquidation (think internet bills, fire insurance, ..), but they still have to pay the accrued liabilities. And finally the debt on the balance sheet is discounted, they paid $17m to settle it - another million.

DeleteI think you should shave off at least a few million of your estimate (probably $4m+ to be fair, and divide by ~69 or something like that. (57.2m shares, 11.1m warrants, 1.3m unvested RSU's that will probably vest) or you are bound to be disappointed.

My own back of the envelop estimate is ~$5.5m left for distribution or ~$0.08 per share.

I maybe missing something, but Pg. 8 on the 9/30/22 10Q can see the warrants being added into the share count of 57 (in '21). For the unvested RSU's, I believe at least a part of that $ amount would have been included in the intra-quarter severance charge, so shares should be in the share count but also would reduce the dollar expense.

DeleteI think you are correct with regards to the RSU's. I didn't include additional costs for the accelerated vesting in my calculations, just increased the share count. Note that the RSU SBC costs are recognized over time, so the unvested RSU's were not included in accrued compensation yet in Q3 2022.

DeleteThe warrants are not included in the share count. Several ways I could explain this but the simplest way is this. In 2021 the company issued 8.3m shares and 7.1m warrants in April. Check the balance sheet of the 2021 AR. The share count increased from 48.3 to 56.7m shares. The new share count includes the new shares but not the new warrants.

Also, on page 5 of the latest quarterly you can clearly see that the average diluted sharecount is 68.1m.

Thank you, I was completely wrong on share count.

DeleteI would also encourage you to have a look at the SIOX proxy filed today to get a feeling for how quickly these biotech liquidations will burn through cash.

DeleteIn addition to cash burn - which were within my ranges - a big surprise in the SIOX proxy was the cash contingency reserve of $6m - $7m. At ~ 25% of the distributable cash, that's surpisingly high. A few other liquidations have provisioned for ~ $1m. Curious about why SIOX reserved so much?

DeleteThanks for the idea. Is the company at risk of being litigated against by the patients?

ReplyDeleteGood question. They do carry clinical trial insurance, here's the boilerplate language from the 10-K risk section:

DeleteAlthough we currently carry clinical trial insurance, the amount of such insurance coverage may not be adequate, we may be unable to maintain such insurance, or we may not be able to obtain additional or replacement insurance at a reasonable cost, if at all. Our insurance policies may also have various exclusions, and we may be subject to a product liability claim for which we have no coverage. We may have to pay any amounts awarded by a court or negotiated in a settlement that exceed our coverage limitations or that are not covered by our insurance, and we may not have, or be able to obtain, sufficient capital to pay such amounts.

Hard to know what their potential exposure is? But good point, worth calling out too.

Just a word of warning: look at the chart of the previous 'writser pointed to this', DMS, before you act on this one .. FWIW I also don't own this myself, I just flagged it as an interesting situation. Reading the PR you get the impression that a liquidation isn't really a consideration here. And I have mixed feelings about buying biotech dumpster fires in the hope that they strike a good reverse merger deal. Sometimes they pop nicely but on average, consider me skeptical about most of these deals.

ReplyDeleteOn the other hand, if a cash box trades at a 40% discount to cash it can buy some random widget for 130% of fair value and you still end up nicely ahead.

One thing I've been pondering is that it seems potentially even more profitable to figuring out which busted biotech company will announce a strategic review _before_ the fact, rather than trying to squeeze out the last pennies after a company has issued a press release.

It's probably difficult to judge whether management will continue to throw more good money after bad after they have announced some bad results. But in this specific case, the company only had two product candidates, MGTA-117 and MGTA-145. In their latest quarterly they mentioned:

"we announced our plan to more narrowly focus our capital allocation on the MGTA-117 targeted conditioning program, the CD45-ADC IND-enabling activities and the MGTA-145 stem cell mobilization efforts in sickle cell disease while also de-prioritizing other portfolio investments. We made certain reductions in our planned spending related to research platform-related investments in new disease targets, paused certain MGTA-145 investments, including the program’s planned MGTA-145 dosing and administration optimization clinical trial in healthy subjects and reduced planned general and administrative expenses. In connection with these reductions to our planned spending, we also reduced our workforce by 14%."

So they fired some people, paused some investments and focused on MGTA-117. And then somebody died and they had to stop that flagship trial. Is it really so unexpected that they decided to throw in the towel? I guess so, because the stock went up 50% in a day ..

If anybody has some thoughts about predicting / searching these kinds of biotech strategic reviews before they actually occur then I'd love to hear them.

Sorry for posting these sunday night ramblings.

For clarity: when I said I don't own this I ment MGTA. Unfortunately I did own DMS ..

DeleteThanks for the portfolio holdings and watchlist, much appreciated.

DeleteWritser - thanks for you comments and insight.

I thought about that too, however, it seemed simply too speculative to engage in the game of predicting who might look for 'stragetic alternatives'. Biotech seems a capital destructive industry with some pretty dodgy players around the traps. I am led to believe the biotech industry has a disproportionate number of frauds too.

MGTA has made no mention of 'liquidation' as an option that I have seen to date. If I recall correctly, both IMRA and SIOX did mention liquidation and ANGN didn't. IMRA worked out doubly well with a lucrative asset sale (depending on your entry price of course) and then a pop on the reverse merge announcement. SIOX is liquidating. ANGN in contrast tanked after giving away their cash for 33% of another biotech in a reverse merger.

On the balance of probability I think MGTA are likely to reverse merge. I don't know what drives the post merge announcement 'pop' vs 'flop', but looking at how low it traded relative to net cash in the recent past it could be a 'flop' quite easily.

I have looked a few sources but I am not sure of the current level of insider ownership on this one which is important to know. If insider ownership is material (and if it wasn't for the litigation) this one would be more interesting for me personally. If you have a good source for current insider ownership please let me know.

The how to get in before is a good question, in hindsight, you're right, this should have been an obvious one. But I don't know if its a good strategy unless you really have a large basket of them, batting average would be important here.

DeleteAnd I agree with the above comment too, hard to know which reverse mergers are buzzy and which aren't, seems to be just market sentiment. Right now, it might work, three months ago, same reverse merger wouldn't, etc.

Hello,

ReplyDeletedid you have a look at Frequency Therapeutics (FREQ)?

Situation is quite similar, some months ago they dived to 1$ and it was well below cash position, now recovered to around 4-5$ with a redout expected in next few weeks. I see you follow OTIC, but after my research, FREQ approach is better in safety and in case of positive readout, the whole technology platform would allow to pursue many other indications.

I haven't. I'm more interested in the ones that have given up and are looking to sell/liquidate their assets in some form, not the ones that still have a readout or are a true going concern still.

DeleteMGTA clinical programs are dead-ends with likely no redemption value. All now depends on the holders and who wants to take control of the situation. Atlas is the firm in the driver seat but can challengers emerge like in CBIO to drive capital return prior to acquisition/reverse merger? Are the existing sharp penciled capital accountable holders like RA Capital still in the stock? They need more cash to launch a large trial or commercial drug so any possible reverse merger comes with follow-on PIPE pricing credibility. More questions than answers and Captain Obvious says "this will trade higher or lower depending on the market participants' responses."

ReplyDeleteAll good thoughts, thanks, I've sized all these sufficiently small to start where I don't need all the answers. As it unfolds, if it looks like a better bet, then I'll add more.

Deletenote 8k filed...pulled the plug.

Deleteseems like net positive to me, cash burn decrease, maybe the can hold the line at $100mm

Deletepositive--yes, the burn is stopped. $100m---doubtful, but $80+ looks better....always the reverse merger ghosts out there that may want that $$

Deletemo money, better biotech reverse merger partners - The Notorious B.I.G, probably

Deletewouldn't they need those executives to help identify reverse merger target? Unless it's already decided.

Deletereverse merger with atlas co - https://www.youtube.com/watch?v=gUhRKVIjJtw

DeleteNo, they don't need the executives. Advisors will run the process for the board.

Deletesome decent sized sell prints out there, who's getting out?

DeleteI've been selling and buying

DeleteDefinitely not your Grandma’s net-nets. Theoretically it makes a lot of sense to buy a company at half cash that could have an approved drug or salable assets. In practice it’s been incredibly hairy. Solidly positive investing returns in the sector so far but it’s been far from easy. With 4-5 home runs 100-200% returns, numerous white knuckle break even or slight gainers 0-25%+ and several -25% or so decliners.

ReplyDeleteSeems like they've booted the exec team and they're shutting up shop ?

ReplyDeletehttps://www.fiercebiotech.com/biotech/magentas-c-suite-heads-out-door-85-staff-closing-process-gets-underway

https://www.bizjournals.com/boston/news/2023/02/03/magenta-therapeutics-shutdown.html

So what is it worth in a liquidation scenario... ?

That's the scenario I describe in my post, estimate ~$1.38 in proforma net cash. As others mention, there could be additional expenses in a liquidation, see SIOX for what that might look like.

DeleteAny thoughts regarding Tang Capital Partners 9.7% stake?

ReplyDeleteNot really. I don't think too highly of him after the APVO and ODT situations.

DeleteTang likes to Bang stocks around.....he's not a serious long-term biotech investor, he's a trader, market dynamics opportunist, likes to make plays with volatility

DeleteYou still long $MGTA and any new thoughts, how long we might be waiting for a deal?

ReplyDeleteYes, still long. No new thoughts, nothing has really happened since my post. Timing, anyone's guess, maybe 6 months?

DeleteYes, it could take a while, I suppose. Thanks for the response.

Delete10k filed today.

ReplyDelete1) they have $36M or so with SIVB, don't believe it is an issue given fdic has guaranteed it, but might spook some folks

2) 84% of staff termed at end of feb $5.4m cost (think this was already in an 8-k).

3) wedbush fee a min of 1% of any transaction or $1.5M,

4) the lease seems to be a big piece here. $39M payable over next 6 years or so. Seems they PV at 11% for their balance sheet liability - $29M. If the landlord had someone lined up I'm sure they may accept that but if not I'd expect it to get discounted at a lower rate (I'm thinking about it kinda like a CMBS loan defeasance but could just be way off). Appears they may have already been sub-subleasing some space to April '24

5)

So is the new math - $112mm cash - $30mm lease liability - $2mm additional severance (guess) - $25mm (2 additional quarters of cash burn, maybe I'm a bit aggressive here) - $1.5mm wedbush fee = $53.5mm. Over 60.639mm shares = $0.88. That seems like the "floor" in a liquidation?

Deletewritser pointed this out in a tweet as reason to believe reverse merger much more likely than liquidation now, any thoughts on r/r now? from most recent 10K

ReplyDeleteOn February 6, 2023, the Company entered into an agreement with Wedbush Securities Inc (“Wedbush”) to act as the Company’s exclusive strategic financial advisor in connection with a potential strategic transaction including but not limited to an acquisition, merger, business combination or other transaction. Upon the consummation of such transaction, the Company agreed to pay Wedbush a success fee of 1.0% of the transaction value with a minimum fee of $1.5 million.

The company also established a poison pill provision. Not a good look for management.

DeleteAdditionally, reading through the risks items, it seems M&A seems a more plausible path rather than liquidation... "If a strategic transaction is not consummated, our board of directors may decide to pursue a dissolution and liquidation."

DeleteYes, I agree, in my post I mentioned they would first try to pursue a reverse merger. If that doesn't work, a liquidation. The poison pill doesn't bother me too much, might be looking at what's going on over at QNCX and not want their hand pushed one way or another.

DeletePersonally, I prefer the cases where a liquidation has already been announced (e.g., CBIO, OTIC, SIOX, MTCR, etc.) Isn't a value-destroying reverse merger the most likely outcome now? It might look a lot like the SESN-CARM reverse merger, where the shares fell >40% since CARM started trading. The poison pill just makes it that much harder to stop a bad deal.

DeleteI think everybody (in value circles at least) prefers a clean liquidation. But that’s why SIOX trades at a very small discount to its distributable cash while Magenta is trading at a much larger discount. A bad deal is already priced in. So if it trades up on announcement, like for example Imara, you’ll end up owning a home run. Whereas with OTIC a successful liquidation is already priced in, so you’re getting shafted if some lawsuit pops up or whatever. I’m not saying I prefer MGTA to OTIC or vice versa. All I’m saying is that with situations like these price matters first, before your personal preference.

DeleteI agree with Writser. In the back of my head I keep thinking there are now so many of these in the same situation, one would think that would lead to more pursuing a liquidation, but we'll see. I assume the biotech community is pretty tight, they run in the same social circles, have a desire to raise cash for each other and discover new therapies, etc., so the reverse-merger path is going to be option #1. But markets have changed, reverse-merger pops seems muted to negative recently, maybe we get more liquidations out of this busted biotech vintage. At least that's the bull case.

Deletelease canceled for $15m...+5 of severance.

ReplyDelete$112 at 12/31-$20=right in that $80ish range now

Whoops, underestimated that breakage roughly in half. But glad to see things are moving along.

DeleteI think you made it back by overestimating 2Qs of burn...they should be at minimal burn from here

DeleteAnyone ever seen a liquidation like MTCR OTIC SIOX get screwed up and shareholders to initial payment or through the end of contingency reserve get screwed?

ReplyDeleteMaybe not get screwed, but several have been disappointing. Maybe the worst was NYRT, but that was a larger REIT liquidation. But yeah, need a certain personality to get into these ideas, patience, okay with limited disclosure post liquidation trust phase, etc.

DeleteWhen you say disappointing can you elaborate? What happened with NYRT? Thank you for sharing your experience.

DeleteDisappointing meaning just the low end of the distribution range or took too long, time often drags down the IRR of these things.

DeleteNYRT was a New York City focused office REIT, it was a popular liquidation play several years back, it was an activist play where the distributions have come in well below the expectations the activist put out there, plus they put their largest asset in the non-traded liquidating trust, covid happened, its an outdated office building, overall results there are going to be pretty poor.

Merger with Dianthus announced, will be interesting to see market reaction, and find out more from the webcast. Not that easy to assess deal based on information in press release.

ReplyDeleteUnderwhelming....doubtful shareholders will approve this one.

ReplyDeleteAgree seems quite unlikely to get shareholder support as outlined so far. If the $70mm of outside capital Dianthus is looking to raise is contingent on the reverse merger hopefully they have adequate incentive to improve to a better-than-liquidation set of terms promptly. Compare this to the IMRA deal not too long ago where there were lock ups etc clearly designed to make the deal actually attractive to shareholders.

DeleteOne has to appreciate that MGTA agreed to pay $13.3m to Dianthus in case shareholders vote down the deal, if I read the merger agreement, page 82, correctly.

Deleteoh ya....who the heck did the negotiating for MGTA?

DeleteI read that as they have to pay that 13.3mm termination fee primarily if entering an alternate merger within a 12mo window or if the board fails to endorse this Dianthus deal. Do you read it as they have to pay that if shareholders vote down the deal and then choose to liquidate? 10.3(b) and 10.3(c) seem most relevant, very possible I'm not reading it correctly.

DeleteGood question, I wasn't 100% sure, that's why I said if I read it correctly. I think section 10.3(b) is relevant, read it again and I think it's an AND of i, ii and iii. So you are probably right.

DeleteConfirmed this point with management, the termination fee would not be owed if shareholders reject the deal and a liquidation follows. In the S-4 a 1.05-1.07 proceeds liquidation estimate is outlined by management.

DeleteVote to block

ReplyDeleteReads as if the target MGTA net cash balance at merger point is only $60m, fair bit below my expectation (closer to $80m). Does anyone understand why it would be at that level?

ReplyDeleteManagement took the money to setup for their severance and next steps

DeleteEstimated close of merger is in Q3 - think that's the main difference (additional burn from EOq1 net cash of ~77 M Net )

Deletehttps://capedge.com/news/benzinga/32185400/mgta-stock-alert-halper

ReplyDeleteHas anyone been able to talk to IR or management? I've reached out several times with little luck...

ReplyDeleteThey've gone under ground, which makes sense, after proposing such a disgusting deal

DeleteAccording to S-4, looks like Tang tried to make a cash offer like Jounce.

ReplyDeleteYeah, maybe he does something similar here. He's a wildcard, no clue what he's thinking ever.

DeleteGiven the hefty 13.3m termination fee pre-vote, I'm assuming he'd have to engage post vote - if he engages. What's a fair dissolution value at the end of Sept? Assuming vote in late July then two months for a strategic alternative to consummate.

DeleteAh true, maybe he just puts more pressure on the liquidation path.

Delete