First Horizon Corp (FHN) ($5.3B market capitalization) is a fairly vanilla regional bank serving a balance of both commercial and consumer customers in 12 states throughout the demographically desirable southeastern United States. Unlike other troubled banks, their clientele is less chunky, less hot money, less return motivated. First Horizon doesn't have customer concentration in asset managers, investment funds, tech start-ups or a large wealth management practice where deposits are less operational in nature. It's just a boring middle American bank with a history of above average, low-to-mid teens ROE.

Back in early 2022, First Horizon agreed to be bought out by TD Bank (TD) for $25/share plus a small ticking fee, however on 5/4, the two banks mutually agreed to terminate the merger due to regulatory approval timing uncertainty. It was later reported by the WSJ that the OCC had concerns about TD Bank's anti-money laundering policies and blocked the deal. The merger arb spread had already widened ahead of the termination signaling the market was highly skeptical of this deal going through, but shares tanked anyways as merger arb holders are selling shares at a time when there are few enthusiastic buyers of regional bank shares to match the liquidity. As of this writing, shares trade around $9.60, less than half of where TD was prepared to take it out.

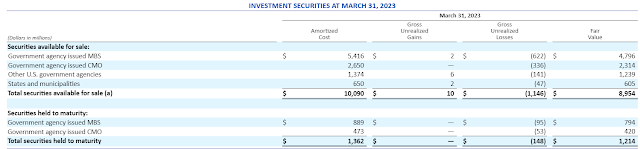

The current banking crisis is different than 2008, there's less concern about the ultimate recoverability of securities on bank balance sheets (AAA CDOs for example, weren't AAA, but there isn't that question with agency MBS), rather the market is more worried about the mark-to-market losses in bank held-to-maturity ("HTM") portfolios if banks are forced to sell securities to meet deposit outflows. First Horizon's use of HTM accounting is relatively small (just 12% of the securities portfolio), deposits (which totaled $61B as of 3/31) large and small would have to flee in mass before the bank would need to realizes losses in their HTM portfolio.

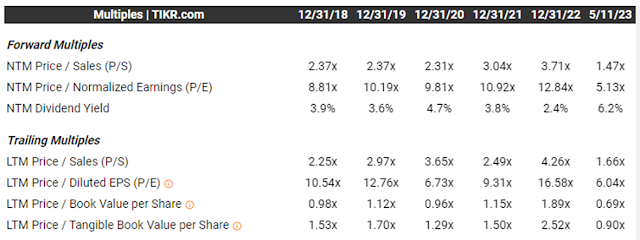

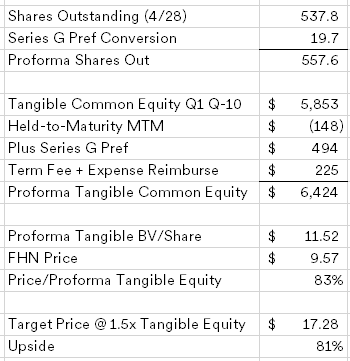

What could FHN be worth once all the clouds clear? Prior to 2022, First Horizon traded around ~1.5x tangible common equity.

- Prior to the termination, some rumors were floating around that TD was looking for a price cut due to market conditions, but First Horizon management stated on their investor call that TD never broached the subject.

- The TD-FHN merger happened due to an unsolicited offer, the bank wasn't running a sale process, so it is unlikely FHN will get scooped up by another bidder in the near term, but also means the board and management take their fiduciary responsibility seriously and would consider other bidders.

- Duration of the investment portfolio is only 5.2 years, each quarter that passes some of the losses will flip as par is realized. The Federal Reserve also appears to be done hiking which should put a floor on the securities portfolio losses.

Why do you think 1.5x tangible book is fair value? Many many banks trade at or below TBV. (Bonus: I didn't dig much, but I can see they believe their loan book is worth carrying value? Is that reasonable? Or accounting jibberish from market the whole thing level 3?)

ReplyDeleteIt's an old saw, 10% ROE = 1x BV, 15% ROE = 1.5x BV, etc. Loan books are a black box, but since 2008 banks generally have been prohibited from making silly loans. Most of the risky lending takes place in non-banks, either in the leveraged loan / CLO market or direct/private lenders. None of that is really in the banking system. I don't think of the southeast as a place where there's a concentration of risky borrowers like a SVB or others.

DeleteHow did you determine mark-to-market losses for the HTM portfolio?

ReplyDeleteIt is in the first screenshot I posted.

DeleteI understand the reason the merger did not go through was not anything wrong with FHN but with TD Bank. FHN is unfairly being painted with a negative brush, where people should be looking at TD Bank and the reasons why adm did not what this merger to go through. FHN is a perfectly good bank caught in the cross hairs of US and TD Bank. For networks like CNBC to lump FHN with other "supposely" trouble regiionals is crazy.

ReplyDeleteObviously I agree. Banks do rely on confidence to a certain degree, and people still remember 2008 well, but I think this crisis is different, depositors aren't at risk.

DeleteWhat about rising deposit costs vs their mostly fixed interest income?

ReplyDeleteSure, their NIM will "normalize" which is bank speak for contract. But 60% of their loan book is floating rate, they don't really bank asset managers, investment funds, others that are particularly return sensitive and/or sophisticated. I think it is manageable.

DeleteGenerically the banks that don’t have long duration securities portfolios, promoted floating rate loans, grew deposits during the first quarter and earn a decently large amount on assets are probably going to do fine. Return on assets of a blended 6% is probably a minimum unless you have some view on interest rates.

ReplyDeleteThe crazy thing is you don’t even have to go to the eye of the storm because everyone has freaked out so much. Even ECIP banks are down a lot which is patently ridiculous because many received “free money” from the government eclipsing their market caps.

6% ROA. Lol. 🥳

DeleteNot ROA. Just looking at the yield on assets. Without netting any expenses.

DeleteDo you have any idea if the bank has any advantage that differentiates it’s self from other regionals?

ReplyDeleteNot really, regional banking is generally a commodity business. Relationships help, the TD Series G preferred that went to fund retention bonuses likely kept most of the talent. But no, I don't see a real moat here.

DeleteNo opinion on FHN (looks interesting based on the above!), but I have been looking at PCB. I think having a large Korean-speaking staff and clientele makes some deposits potentially stickier. They have done very well, though I'd certainly understand nervousness given their business and location. Have also started to look at SLRK, which I recall struck me as a very well-run bank a while back. I think the local-bank trade may (/will) have a lot more downs first, but will likely look like a no-brainer in retrospect in 3-8 years. People talk about GFC & the S&L crisis, but those had much more excessive excesses, IMO. Could be wrong! Probably am!

ReplyDeleteI'll take a look at PCB, sounds interesting. Similarly, FHB has a sticky deposit base for cultural reasons too, everyone knows the BOH story, but FHB is essentially the same but with less HTM losses. Hawaiians hate outsiders, seem unlikely to move their deposits to a mega mainland bank.

DeleteAnother similar bank NRIM ,Alaska based bank but only down 25%from pre crisis

DeletePCB also got some ECIP funds and is doing all the right things (if that can be said of any bank). FHB very interesting!

DeletePCB's ROEs in 2008 were horrendous. I agree this crisis is very different, but I worry about the quality of their current loan portoflio when they showed poor management in 2008.

DeleteI think there's plenty to be worried about in their current portfolio if you're so inclined. I do think this crisis is different enough from 2008, and they're a significantly more seasoned org (they were only a few years old then, no?) that I'm not sure it's super-dispositive. Which isn't to say they can't come up with a new way to lose money.

Deletethere are banks I have bought over the last few weeks I have been looking for banks near book value without large exposure to commercial real estate or HTM exposure, loan to deposit ratio under 90%, stable deposits, and good history

ReplyDeleteThe banks which I bought were (in position size order) HBAN OZK UMBF HIFS MTB ( my local bank) SMBK CCBG EBTC FBK

Also all these banks have NIM over 3

DeleteSorry if this becomes HIFS hijacking another value thread. HIFS misses on most of the criteria you mentioned, mainly commercial real estate exposure and low leverage. It certainly screens as cheap if you don't assume any losses that reduce book value. How did you get comfortable with their ability to weather the storm while the variable interest rate portion of their loan book reprices?

ReplyDeleteyes my bad HIFS was a stock I bought a bit earlier, because the CEO has a long history of being one of the better bankers in the country

DeleteThat one and OZK were the ones I bought due to confidance in the CEO rather than finding them from a screen

DeleteDeposits are not just fleeing regional banks because they are afraid of solvency, but to get better yields from money market funds. People didn't care about incremental gain in the past, now they realize the difference between savings accounts and mm accounts is significant. All this turmoil is in the banking is making people aware of the difference. How can anyone peg that risk?

ReplyDeleteevery bank I listed had more or less stable deposits through March .

ReplyDeleteSince you're asking, I'll say that ALLY has been punished also. Although not classified as a bank (more like Credit Services), it is one (bank charter and all). Their deposits are very sticky since they've been paying good interests to their depositors for a long time. I believe it's their assets side that people misunderstand. It's mostly prime car loans. People assume those loans will sour. I think the reserves are more than sufficient (but that's just my opinion). Sells under book value, even after all the mark-to-market adjustments that occurred during the last year.

ReplyDeleteI don't mind auto loans, people pay their car payment before their mortgage. Need a car to get to work and it is less politically sensitive to repo a car than to foreclose on a home, much easier process.

DeleteOn ALLY and other internet banks, not sure their high interest rates is a positive. I'd prefer banks where the depositors are there for non-investment return reasons, they're more operational accounts than savings accounts. Because online banks can be as competitive or more competitive since its easier to switch.

Thanks for the idea!

ReplyDeleteThanks for the idea. Any reason to worry about the lost noninterest-bearing deposits? Fell 10% last Q from 23 M to 21.

ReplyDeleteNot a reason to worry more than banking in general. QT is pulling deposits from banks in general.

DeleteI crossed over LTCG and sold. Still think this one would make a good acquisition for one of the super-regional banks wanting southeastern exposure.

ReplyDelete