As the market continues to make new highs it's getting more and more difficult to find value in mainstream equity securities. Most potential investments that interest me have a bit of hair on them, one that has recently appeared on my radar is Calamos Asset Management (NASDAQ:CLMS, but I'll refer to it as CAM). I should probably wait another week for their 1st quarter results to come out, but I haven't posted in a little while and wanted to get something out here.

John Calamos started what would become Calamos Asset Management in 1977 by taking out a home equity line of credit and focusing on convertible bonds. Today Calamos is a vanilla multi-strategy asset manager with $30.6 billion in assets (as of 12/31/12) based out of Naperville, Illinois, a western suburb of Chicago. After graduating college in the early 2000s, I actually interviewed for a position at Calamos and subsequently didn't get hired, probably ended up being a smart move on their part, no hard feelings.

Calamos was a darling of the late 1990s and early 2000s posting some stellar returns. Management took advantage and went public in 2004, they had a couple of good years and peaked with the market in 2007, since then they've struggled with mediocre to poor performance in their flagship Calamos Growth Fund and the Calamos Growth and Income Fund. Both have seen significant drops in assets due to both losses in the portfolios and investor outflows. In 2007, Calamos Growth Fund had over $15 billion in assets, today it has $5.2 billion and has badly trailed the S&P 500 over the past 2 years (+9.33% vs +16.00% in 2012, -9.07% vs +2.11% in 2011) and continues that trend in 2013.

On the bright side to the poor performance of their growth fund, Calamos has been forced to diversify their business model and focus on a variety of strategies potentially making their go-forward revenue streams less sensitive to the fortunes of one portfolio. And despite all the recent struggles, Calamos' operating margins have remained pretty steady in the 35-40% range, showing their ability to right size expenses as assets have come down since 2007 (also might shoot holes in the potential argument that if assets increase, Calamos would have a lot of operating leverage).

John Calamos started what would become Calamos Asset Management in 1977 by taking out a home equity line of credit and focusing on convertible bonds. Today Calamos is a vanilla multi-strategy asset manager with $30.6 billion in assets (as of 12/31/12) based out of Naperville, Illinois, a western suburb of Chicago. After graduating college in the early 2000s, I actually interviewed for a position at Calamos and subsequently didn't get hired, probably ended up being a smart move on their part, no hard feelings.

Calamos was a darling of the late 1990s and early 2000s posting some stellar returns. Management took advantage and went public in 2004, they had a couple of good years and peaked with the market in 2007, since then they've struggled with mediocre to poor performance in their flagship Calamos Growth Fund and the Calamos Growth and Income Fund. Both have seen significant drops in assets due to both losses in the portfolios and investor outflows. In 2007, Calamos Growth Fund had over $15 billion in assets, today it has $5.2 billion and has badly trailed the S&P 500 over the past 2 years (+9.33% vs +16.00% in 2012, -9.07% vs +2.11% in 2011) and continues that trend in 2013.

On the bright side to the poor performance of their growth fund, Calamos has been forced to diversify their business model and focus on a variety of strategies potentially making their go-forward revenue streams less sensitive to the fortunes of one portfolio. And despite all the recent struggles, Calamos' operating margins have remained pretty steady in the 35-40% range, showing their ability to right size expenses as assets have come down since 2007 (also might shoot holes in the potential argument that if assets increase, Calamos would have a lot of operating leverage).

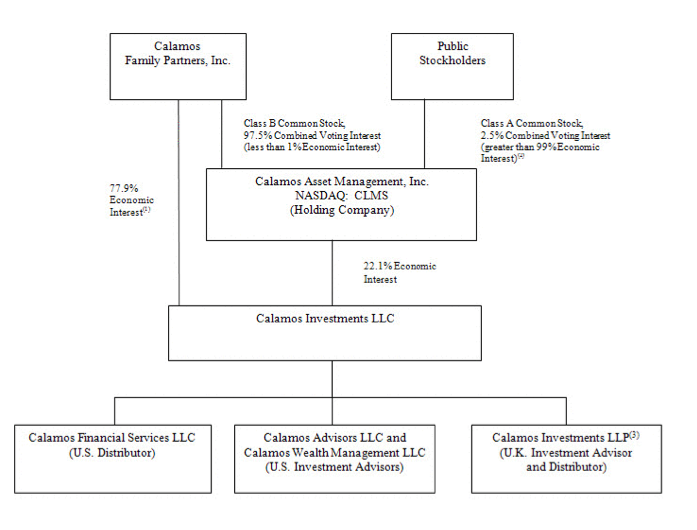

Corporate Structure

In addition to their poor performance, Calamos has a complicated corporate structure that obscures the true underlying value. The public stockholders have a 22.1% economic interest in Calamos Investments LLC, a partnership where the operations take place, and the remaining 77.9% is owned John Calamos and his family through Calamos Family Partners, Inc. Additionally, Calamos Family Partners owns all the Class B Common Stock of Calamos Asset Management giving them 97.5% of the voting power, the family is fully in control of their namesake company. Below is the graphic provided in the 10-K.

This structure makes it difficult for investors to fully capture what the entire Calamos Investments entity is worth as most financial software will list the market capitalization as just the 22.1% CAM interest, even though the family can convert their ownership position to Class A shares under certain circumstances. The corporate structure also obscures the assets held at the CAM level because Calamos Investments is fully consolidated with CAM in the financial statements. In addition to the 22.1% ownership in Calamos Investments, CAM has the below "Other Assets" as outlined in their filings:

Sorry if that's a bit hard to read, but to summarize, CAM shareholders have a sole interest in $67.6 million in cash and tax receivables, plus a net deferred tax asset of $55.3 million, discounting the DTA and the combine total is worth $105.4 million or $5.17 per share to CAM. That's 46% of the current price of $11.20 per share, so it begs the question what's the 22.1% of Calamos Investments worth?

Valuation

First let's take a look at the balance sheet value of Calamos Investments' liquid assets, which is pretty straight forward:

Cash = $39.2 million ($106.8, netting out the $67.6 million attributable solely to CAM above)

Cash = $39.2 million ($106.8, netting out the $67.6 million attributable solely to CAM above)

Investments = $349.4 million

Partnership Investments = $60.8 million

Debt = $92.1 million

Net Position = $357.2 million

CAM's share = $357.2 million * 22.1% = $78.96 million = $3.87 per share

In 2012, the pre-tax operating earnings of Calamos Investments was $119.8 million (or roughly 1% of assets under management, in line with their historical results). Most asset management firms trade for something close to 10x pre-tax earnings, but given the recent performance struggles and odd corporate structure, let's give them a discount of 8x pre-tax earnings. At 8x $119.8 million, the fee income stream is worth $958 million to Calamos Investments, or $211.7 million to CAM, $10.39 per share.

Conclusion

Add up the three pieces, and CAM's fair value should be close to $19.43 per share compared to today's price of $11.20. Another way to look at it, the market is only valuing the $26.47 million pre-tax annual CAM revenue stream at $44.03 million. Or on an after tax basis, the market is giving the fee business a 2.5 P/E (($11.20-$3.87-$5.17)/($0.88 diluted EPS)). Calamos also pays a $0.125 quarterly dividend (roughly ~4.5% annualized) to shareholders while you wait for the valuation gap to close.

The dissenting view on Calamos would ask why the valuation gap would ever close? Calamos Family Partners is getting its pro-rata share of the taxable income from Calamos Investments and at this point the family doesn't appear to have a pressing need for CAM's valuation to catch up to intrinsic value. However, I'm a believer that value can be its own catalyst and CAM is clearly undervalued. Any signs of the "great rotation" into stocks by retail investors coming true could also improve investor sentiment around traditional asset management firms.

Disclosure: No position in CLMS, but may add soon if I can free up some cash

In 2012, the pre-tax operating earnings of Calamos Investments was $119.8 million (or roughly 1% of assets under management, in line with their historical results). Most asset management firms trade for something close to 10x pre-tax earnings, but given the recent performance struggles and odd corporate structure, let's give them a discount of 8x pre-tax earnings. At 8x $119.8 million, the fee income stream is worth $958 million to Calamos Investments, or $211.7 million to CAM, $10.39 per share.

Conclusion

Add up the three pieces, and CAM's fair value should be close to $19.43 per share compared to today's price of $11.20. Another way to look at it, the market is only valuing the $26.47 million pre-tax annual CAM revenue stream at $44.03 million. Or on an after tax basis, the market is giving the fee business a 2.5 P/E (($11.20-$3.87-$5.17)/($0.88 diluted EPS)). Calamos also pays a $0.125 quarterly dividend (roughly ~4.5% annualized) to shareholders while you wait for the valuation gap to close.

The dissenting view on Calamos would ask why the valuation gap would ever close? Calamos Family Partners is getting its pro-rata share of the taxable income from Calamos Investments and at this point the family doesn't appear to have a pressing need for CAM's valuation to catch up to intrinsic value. However, I'm a believer that value can be its own catalyst and CAM is clearly undervalued. Any signs of the "great rotation" into stocks by retail investors coming true could also improve investor sentiment around traditional asset management firms.

Disclosure: No position in CLMS, but may add soon if I can free up some cash

Two years later and stock is $9 with 6% yield. Any thoughts on getting in at the moment?

ReplyDeleteI've only loosely followed the story, but just doing the same back of the envelope math I get somewhere in the same neighborhood (assets attributable to CAM have gone up, pre-tax income down), so it's trading around 50% of it's intrinsic value. But I don't see the complex corporate structure changing anytime soon, the Calamos family could wake up one day and decide to sell, but it's unlikely. The active mutual fund business is in permanent decline, not entirely sure why they've bulked up their expenses in that environment, gives me the perception the company isn't run for the public shareholders. But certainly a cheap stock. Thanks for the comment.

Delete