Full warning, similar to Armstrong Flooring (AFI), this could be a terrible idea, it has significant red flags and is highly speculative.

LMP Automotive (LMPX) is a micro-cap (~$45MM market cap) that came public in late 2019 with a car subscription model where users could rent a car month-to-month, positioning itself as splitting the difference between a short-term car rental and a traditional car lease. LMPX then put an online dealer/mobile app business model spin around it to market the stock. In 2020, LMPX became a bit of a meme stock, briefly trading up alongside other e-commerce car dealers like Carvana, but then crashed as they were unable to source cars economically to run their subscription model. Instead, the company pivoted to be a traditional car dealership rollup business and went on a debt fueled acquisition spree in 2021. LMPX finished the year with 15 new car dealerships and 4 used car dealerships across 4 states. On 2/16/22, the company said they were unable to secure new financing for their previously announced but not yet closed acquisitions (7 of them!) and quickly pivoted to pursuing a sale:

Sam Tawfik, LMP’s Chief Executive Officer, stated, “The Company intends to terminate all of its pending acquisitions in accordance with the terms of their respective acquisition agreements, primarily due to the inability to secure financial commitments and close within the timeframes set forth in such agreements.”

“The Board of Directors believes that LMP’s current stock price does not reflect the Company’s fair value. Given the record M&A activity in our sector and multiples being paid for these transactions, LMP’s Board of Directors has directed management to immediately pursue strategic alternatives, including a potential sale of the Company.”

The stock closed at $5.25/share on 2/16, it now trades for ~$4.25/share.

Putting aside terminal value questions (auto OEMs bypassing dealers, electric cars needing less maintenance), car dealerships are fairly high cash flowing business and were big covid beneficiaries. There is a lack of supply (nationwide, dealership inventory is ~1/3rd of normal, going to take a while to normalize) that has raised prices and reduced the need for car salespeople (dealerships have been slow to rehire those laid off during the pandemic) as more people browse online and the low inventory has all but eliminated haggling. Car owners are also holding onto to their cars longer creating more high margin service revenue. Some of these covid changes may be lasting, many dealers talk about inventory being permanently lower as dealers become more of a distribution center and less of a place where people walk the lot to find the car they want, they've already decided on the specs online before going to the dealer.

There are thousands of dealerships across the country, they're reasonably liquid assets that change hands regularly (similar to why I like REIT special situations, the assets are fungible and there's a large pool of buyers). Here, there are 7 large publicly traded dealership groups (KMX, LAD, PAG, AN, ABG, GPI and SAH, but only ~10% of all dealerships) and many other large private ones. The windfall profits of the last few years has prompted the larger public players to do a lot of M&A, rolling up this fragmented market. While large dealership groups are thriving, many smaller dealerships are struggling to source inventory and are at risk of failure, in order to press their scale advantages, the big are getting bigger. Awkward long way of saying, I don't think LMPX will have trouble finding buyers for their dealership assets, but it is more a question of price.

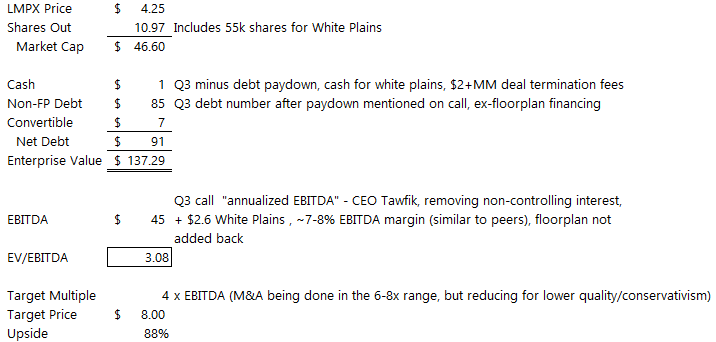

Given the rapid rollup nature of LMPX, nailing down the valuation causes a bit of brain damage to work through the financials, here's what CEO Sam Tawfik said in the Q3 earnings call:

Our third quarter annualized run rates excluding the acquisition we closed this quarter, which we expect to be immediately accretive to income this quarter are $565 million in revenue, and $47.6 million in adjusted EBITDA.

The acquisition referenced above is the White Plains Chrysler Dodge Jeep Ram Dealership that closed in October, purchased for $19.2MM that was estimated to generate $2.6MM in 2022 EBITDA.

Then in the company's annual letter on their website, Tawfik provides:

We completed the acquisition of our contracted White Plains, New York Chrysler Dodge Jeep Ram in the early fourth quarter using approximately $5 million in cash from the company’s balance sheet, 55,000 shares of common stock and $1.3 million in cash from our existing credit facility. This acquisition will be immediately accretive to earnings in the fourth quarter of this year. As a result of this year’s acquisition activity, the company currently owns 15 new vehicle franchises, operates 4 pre-owned stores across 12 rooftops in 4 states which generate over $600 million in annualized revenue.

Later:

We intend to pay down our existing term debt by approximately $11 million in the fourth quarter of 2021, resulting in a balance of approximately $85 million, of which the company allocates $53 million to its real-estate holdings and $32 million to its dealership blue sky purchase debt. Essentially at the current pace of cashflow generation, if we choose, the company can extinguish its current blue sky debt in less than a year.

Adding it up together:

Risks/Red Flags:

- Obviously, top of the list, LMPX went on a crazy acquisition spree in 2021 and couldn't raise capital to complete them (credit conditions have tightened slightly this year, but still pretty open). Most of these deals included a combination of debt and stock, struck when the stock was $15-$17, by the time it came to close these transactions the air was being let out of the growth balloon, the stock was $7 and the window to raise capital closed on LMPX. Buying dealerships at 7x EBITDA while the stock trades well below that doesn't make much sense. It could be nastier than that simple explanation under the hood, but the Q3 numbers look fairly decent, this is a mess but was at least cash flow positive during the last reported quarter.

- Tawfik owns approximately 35% of the company, he appears to be the sole decision maker and doesn't seem to have a strong board around him. There are a number of related party transactions, none appear overly egregious but in total they don't look great, plus in October, Tawfik bought a company plane for himself only a few short months before it all fell apart. His biography includes founding Telco Group which was sold to Leucadia back in 2007 for $160MM and also founded PT-1 Communications which was sold to Star Communications in 1998 or $590MM. Presumably he's not totally incompetent but might have just gotten caught up in the market hysteria last year.

- Tawfik has been selling a small amount of shares regularly as part of a 10b5-1 plan, I'm not an expert on these insider selling plans, not sure if they can be cancelled halfway through, but it is not a great look if you think the stock is materially undervalued.

- LMPX reports EBITDA per share versus enterprise value, that's always a red flag for me as it is intentionally comparing apples to oranges.

- Their current term loan matures in March 2023, so they've got a little time to get this process done and less of a forced sale than AFI.

Disclosure: I own shares of LMPX

Good write up. What is this worth if car prices normalize and there is no sale? IE what is normal CF for this business? Trying to figure out downside if there is no deal!

ReplyDeleteIt's a fair question, I don't really have an answer. I think the standard view is the car industry is not going to normalize for 2-3 years, supply chains might be somewhat back to normal by the end of 2022 but there will be a lot of pent up demand from the short supply, this could be a multi-year environment. I don't know if "no sale" is really an option, like I mentioned in the post, dealerships are fairly liquid, their term loan is due in a year, pretty sure something happens (could be something negative too) in the next year where the business doesn't exist as-is that we need to normalize cash flows too much.

Deletethanks for the v intriguing writeup. i can't get over the mixed signals here. as you said selling stock under a 10b5 whilst running a process and claiming your stock is materially undervalued is insane (if Sam is a rational actor). i believe you can simply cancel a 10b5 and stop selling (correct me if im wrong); why would you not do this?

ReplyDeletealso i am not sure your point about positive FCF in 3Q is correct. if you compare 3Q cash flow to 2Q cash flow, it looks like absent working capital swings (very big) the actual operations burnt cash. at 6m'21 they had generated +11mm of OCF (with a +10mm W/C benefit), as of 9m'21 it was +32mm of OCF but with a +37mm W/C benefit). furthermore it looks like a decent chunk of this W/C benefit is simply not paying bills? (account payables and deferred comp line items)

also it looks like they took out a loan (from the CEO) to finance the purchase of the plane (you mentioned), but again, this happened in 4Q (ie subsequent event), hardly suggestive they are rolling in cash. interestingly the loan to finance the plane from the CEO was struck at favorable terms (no interest??)

all very strange. given the acquired nature of the assets and lack of historical disclosure; the lack of evidence of true FCF; and the conflicting signals from insiders, its very difficult to make heads or tails of it. could really work out in a sale, as you suggested, but there is some risk the numbers aren't kosher here, in my view.

*EBITDA positive yes, should correct that.

DeleteYeah, "very strange" is a good way to characterize it.

Their model of buying only 70% of each operating dealership JV while leaving original owners in operational control (+ buying 100% of the real estate), might be hard to re-sell without a discount. One upshot of the 10b5 sales is a take-under doesn't look like the current intention. If I recall part of the stated logic of the Cambria dealerships take-under in the UK recently was so they could experiment with leasing models.

DeleteLMP has an "interview" posted on youtube when pursuing the leasing model ("LMP Automotive: Disrupting the Multi-Billion-Dollar Auto Industry 2,633 viewsOct 26, 2020").

Good point, maybe they have to do it piecemeal. But there have to be a lot of buyers out there? I keep thinking to myself that dealerships trade all the time, maybe not to dis-similar to a warehouse or apartment building.

DeleteFrom my understanding, car dealerships usually transact at the multiple value plus the inventory. Are we missing the inventory value in this target share price? Also, spoke to an industry expert who guided to 3-5x on used dealerships and 5-12x on the new ones (not deal specific, just generally). Not super helpful given the large range but thought I would pass along.

ReplyDeleteIt is missing inventory, I went back and forth on how to account for that, like I said, first time really looking at dealerships but open to suggestions/push back. Yeah I think the wide range on new dealerships is really location and franchise specific, LMP has most domestic and economy imports like Kia. There's a lot of room here either way, I think the big question is if this is a legit operation and not a bankruptcy candidate.

Deletehttps://www.sec.gov/Archives/edgar/data/1731727/000121390022012639/0001213900-22-012639-index.htm

ReplyDeleteThe plane was sold.

sometimes the dollar amounts are so small it seems like a group of doctors could save these folks

DeleteI mentioned this stock/category a while back, time for a “brief” followup (keep meaning to revive my ancient Wordpress, but I’m lazy & thus just lurk in comments!)

ReplyDeleteMN announced it’s getting bought out at ~.8% AUM, net of cash (all math here is very back-of-the-envelope, so assume I’m off a little). It’s a middling-at-best subscale asset manager that generates a lot of cash (for now), has an excellent balance sheet, and has undergone a transformation where the controlling shareholder was taken out at a very favorable price to put majority ownership into public hands.

The whole category is faced with an existential question: do they really add much value? Erosion by indexing and low-fee products continues, and the question is whether the #1 thing keeping these businesses going is client inertia. On managers’ sides, there’s been a push for better IT, new product offerings, etc., but there’s the eternal question of whether this is good money after bad. It is above my paygrade to game out whether changing market conditions will result in inflows or outflows.

Small managers with what I consider more of a pedigree—Pzena, Gabelli, etc.—trade at 1.1-1.6% AUM, perhaps due both to superior economics and superior results. These are “brand names” who perhaps don’t want to expand too rapidly from their niches. But the name of the game in a fee-pressured world still likely undergoing a secular move toward passive investing is scale/consolidation.

With all that in mind, I think WHG is interesting here. It received a maybe-not-real $25 buyout offer a year ago, rejected it, and has been under pressure from at least one large holder since (last trade $15.39). Maybe in response to this, they issued a $2.50 special dividend from their large cash hoard and increased the regular dividend 50% to 60 cents a year. Their AUM ebbs and flows with the market; their current EV of ~$55 million (market cap of ~$130 million—they have a lot of cash) is ~.4% of their last reported AUM. .8% would yield a stock price in the low 20s, up 40-50% from here.

Worth noting also that their AUM is roughly where it was 2 years ago, when they were paying $1.72/year in dividends (maybe foolishly; reduced from $2.88 and subsequently dropped to $.40 before the recent increase).

This is a case where any news is probably good—if their AUM, great, if they’re doing poorly, it puts more pressure on management.

Basically they are treading water with, I believe, management planning to get back to higher yields to buy off shareholders. The greatest risk is that management—which has a poison pill—will continue to believe they can refreeze the melting cube, rather than giving up and selling out. No specific timing on this, but MN and WDR last year and the ??? offer for WHG all indicate it’s “in the air.”

Thanks for the idea, hadn't heard of WHG before, I'll add it to my list. I do agree with the consolidation theme, maybe more on the larger end but the banking sector is looking for fees and been buying up a lot of asset managers. Maybe that changes with NII perking up a bit with increasing rates, but a lot of banks have been scarred and don't view a dollar of NII the same as a dollar of fees (for good reason).

DeleteI liked this idea, but then heard management on the call mention they were looking to acquire others versus being acquired. Didn't realize WHG was the Wedgewood that lends their name to the Teton funds, which I saw was also pursuing strategic alternatives, but that one is extremely illiquid.

DeleteMaybe WHG buys them?

DeleteTo be clear, MN was the stock I mentioned a while back, I think, not WHG. But I think WHG rhymes, as noted above. And I still think there might be room for a slightly increased offer on MN. I'm happy enough with $12.85, but had penciled in $14.

ReplyDeleteDid you include the proceeds from the sale of the plane? Apparently sale was concluded today for $6.7 mn.

ReplyDeleteI didn't, not directly, I'd bucket it in the back of the envelope fudge factor valuation.

Deletethank you

ReplyDeleteTHANK YOU

ReplyDeletehttps://seekingalpha.com/pr/18751711-lmp-automotive-holdings-inc-provides-corporate-update-and-announces-will-delay-2021-financial

ReplyDeleteLMPX has $30MM of cash as of 3/31 and $85MM of debt, so an EV somewhere around ~$110MM. Seems very cheap despite all the red flags.

What do you think of the delayed filings? I'm surprised we haven't seen a strategic announcement.

ReplyDeleteEh, 3 months isn't that long if they were starting from scratch on the strategic process. I'm generally in the camp that things take longer in the real world than investors expect.

DeleteThe news that they have to restate earnings is more of a red flag to me than the delayed filings. I don't trust this management team, but they do keep reiterating how well the business is performing, so I'll continue to hold.

https://seekingalpha.com/pr/18868192-lmp-automotive-holdings-inc-provides-financial-update-and-signs-15_8-million-all-cash?source=content_type%3Aall%7Cfirst_level_url%3Aportfolio%7Csection%3Aportfolio_content_unit%7Csection_asset%3ApressReleases%7Cline%3A1

ReplyDeleteAnother financial update including selling one of their dealerships.

"We believe that our remaining real estate portfolio, which was appraised at approximately $50 million, plus our dealerships, including the Chrysler Jeep Dodge Ram dealership in White Plains, New York that we have contracted to sell, can be worth approximately $104 million based on a modest 0.16 multiple of quarterly annualized revenue."

It is worded a little strangely but I think they mean that the dealerships separate from the real estate is worth $104MM. If that's right, this really could be worth significantly more than it is trading. Just hard to have confidence in it. I did sell a little a ~week ago into little run up it had, but still have a position.

I initially read that sentence as 104M in aggregate between dealerships and land, had to go back to do the math.

Delete"The following are preliminary estimates of our overall dealership portfolio performance for the quarter ending June 30, 2022:

Revenue of approximately $164 million, a 10% increase compared to the first quarter of this year (an estimated $149 million)."

164M rev. Q1 *4 qtrs/yr * .16 multiple of revenue = 104.96 in value attributed to the dealership franchises excluding real estate. Not that you didn't already figure this out, but maybe it helps another reader.

Start with that 104.96, slap on the 36M of cash, back out the 78M of debt, add on 50M for the real estate, and you have a purported NAV of ~112M vs a market cap of ~60M.

Theoretically, these dealerships are cash flow positive in aggregate while awaiting sale, so you still have significant upside at current prices, but man these managers are trying their best to make me avoid going within 100 miles of this with the late filings and restatements, not to mention their sales of shares... Sometimes the "ick factor" is how you make money, but it is never easy to pinch my nose.

Did anyone here get to speak with Mr. Tawfik? Do we think he's an honest man?

I haven't spoken with him. But it does make me nervous, another ick factor is the CFO just resigned and Tawfik is now also the interim CFO along with Chairman/CEO, with what appears to be a very weak board of directors, no strong shareholder, etc.

Delete*CFO was terminated, not resigned.

DeleteHas anyone else looked at the Q3 '21 10-Q and not been able to make heads or tails of the numbers representing the "unaudited pro forma summary in the three and nine month periods ended September 30, 2021 and 2020, respectively, presents consolidated information as if the acquisition had occurred on January 1, 2020"? https://www.bamsec.com/filing/121390021060055?cik=1731727

ReplyDeleteSee page 19 on the Fuccillo Acquisition. If I were Tawfik, I'd annualize Q3 '21 as well if that quarter alone were better than the full nine months in 2021. Keep in mind that dealers were beyond the COVID slump by the beginning of 2021. They were riding a large tailwind rather than headwind. What happened in Q1-Q2? All of the dealerships except Fucillo lost money on a pro forma basis for the 9 months ended 9/30/21.

A quick sanity check is that most of the high quality public dealership trade at 1.25x -1.5x book. Exception is KMX which is a different model (used). Realize there is plenty of nuance that could distort the multiple related to owned real estate, acquisition model, partial ownership, etc. However, a materially higher share price - which I think you need given all the well outlined risks in your write-up - would mean a P/B of ~3x. 3x would be a major premium for a broken, subscale, geographically desperate dealership group.

Sorry, I feel like the above was poorly written. Long story short, I don't think that these dealerships generate anywhere near $45 million in EBITDA on a normalized basis.

ReplyDeleteTwo of the acquisitions were essentially asset sales - (Beckley Buick / GMC / Chevy / Kia) and Bachman. The backup for this is in the "Net Assets Acquired" section of the 3Q '21 10-Q. You could argue that the two deals were negotiated and sold on a TTM basis that included an abysmal 2Q 2020. I still do not think an owner would sell these dealerships for no "blue sky value" if they were generating cash in a normal environment.

The Fuccillo dealerships are quality assets that generate real earnings based on a conversation with another Kia dealer in FL. He believes they were making "$1M a month" in 2021, but take that with a grain of salt. If it's true, that's $12 million of earnings.

That leaves Beckley Subaru and the CDJR dealerships, neither of which I believe are generating much cash.

I want to believe in that $45 million EBITDA number, but a few things just don't make sense.

The 10-Q numbers.

The $38 million of Goodwill and Franchise rights on the BS that somehow bought $45 million of earnings.

The greater than 2x P/B multiple that you would have to put on this company to get a return that matches the risk. Best in class ABG trades at 1.5x

Thanks for the thoughtful comments, I have a bit of post-covid brain so I haven't spent time to fully process your thoughts. But I agree that something is fishy here, but Tawfik keeps putting out these financial updates/statements on how cheap it is. I did cut my position back a bit, but continuing to hold. I'll probably come back with better thoughts at a later time.

DeleteThanks for the comments and the write-up. Came across this blog and was happy to see someone else was looking at LMP. Have enjoyed reading some of the other posts as well. I'm sorry to hear about COVID and hope you feel better!

ReplyDeletehttps://seekingalpha.com/pr/18895132-lmp-automotive-holdings-inc-and-affiliates-enters-all-cash-asset-sale-agreements-and-intends?source=content_type%3Aall%7Cfirst_level_url%3Aportfolio%7Csection%3Aportfolio_content_unit%7Csection_asset%3ApressReleases%7Cline%3A9

ReplyDeleteMight have actually gotten one right. LMPX says the ultimate distribution should be $115-$126, which is $10.49-$11.49ish. I added back to my position first thing this morning.

Good call here, and thanks again for the write-up. Will be good learning to see what I got wrong. Dumb question. Do you know if they are obligated to release the delayed financials after they liquidate? Would love to know if they just timed this perfectly, benefited from paying a low purchase price, benefited from a rapid increase in RE value, or benefited something else that I missed.

ReplyDeleteMy guess is they will be current on their financials prior to soliciting votes to liquidate, so we'll see everything prior.

DeleteWas curious to know how this is rolling out. I saw that they closed the deal for their FL dealerships in December, and should close another one for a couple of kia, WV and Subaru dealerships around March.

ReplyDeleteSeems like distribution of proceeds hasn't started yet, but couldn't (wasn't able to) find what the timing of liquidation is supposed to look like. So I'm wondering what is driving the stock down since Sept and if I'm missing something here.

Any update

I haven't been following it closely because it went dark. I can't buy dark stocks, I'm guessing that is at least part of driving the stock down, most investors can only sell and not buy.

DeleteNow that we have $7.42 in total distributions after mgmt was quoted as saying $10.5-11.5(ish), can anyone shed light on how much stock mgmt owns, or has owned? Even if the remaining value is cut in half, it's a 5x bagger for those that can buy expert market.

ReplyDelete