On a quiet Black Friday, private equity firm Centerbridge Partners filed a 13D on INDUS Realty Trust (INDT) ($590MM market cap) stating they "anticipate submitting a Potential Proposal" to acquire all the outstanding shares they don't own.

Item 4. Purpose of Transaction

The Reporting Persons initially acquired the shares of Common Stock for investment purposes. From time to time since the date of original investment in the Issuer, the Reporting Persons have engaged in evaluations of the Issuer and its business, including engaging in discussions with management, other shareholders and other persons. In connection with their regular review of their investment in the Issuer, and based on current market conditions and other factors, the Reporting Persons have changed their intent. On November 14, 2022, Centerbridge determined to explore possible strategic transactions involving the Issuer, including pursuing a proposal to acquire the outstanding shares of Common Stock not currently held by the Reporting Persons (a “Potential Proposal”) and to communicate with, among others, management, the Board of Directors of the Issuer (the “Board”), stockholders and other stakeholders of the Issuer, potential acquirers, service providers and debt and equity financing sources, and/or other relevant parties regarding the foregoing. The Reporting Person may exchange information with any such persons, which may be effected pursuant to one or more confidentiality or similar agreements which may include customary standstill provisions.

While the Reporting Persons have engaged in evaluations of the Issuer and its business, including engaging in preliminary discussions, the Reporting Persons have not definitively determined to make a Potential Proposal or otherwise with respect to any specific actions regarding the acquiring, holding, voting or disposing of any securities of the Issuer. However, based on the status of their evaluation of the Issuer and its business to date and based on current market conditions, the Reporting Persons anticipate submitting a Potential Proposal to the Issuer. Any such action may be made alone or in conjunction with stockholders and other stakeholders of the Issuer, potential acquirers, service providers, debt and equity financing sources and/or other relevant parties and could include one or more purposes, plans or proposals that relate to or would result in actions required to be reported herein in accordance with Item 4 of Schedule 13D.

The Reporting Persons have not yet determined what the terms of any such Potential Proposal may be and no assurances can be given that any Potential Proposal will be made, that any Potential Proposal, if made, would be accepted or that any transaction contemplated by the Potential Proposal with the Issuer will be consummated. No binding obligation on the part of any of the Reporting Persons will arise unless and until mutually acceptable definitive documentation has been executed and delivered.

INDUS is a pretty simple REIT, they own, develop, purchase industrial/logistics properties and lease them out on a triple net lease basis. Despite concerns that Amazon is pulling back on their warehouse spending spree, demand for industrial properties remains high and cap rates low, according to INDT CEO Michael Gamzon (from BamSEC) on their recent Q3 earnings call:

William Thomas Catherwood BTIG, LLC, Research Division – Director & REIT Analyst

Appreciate that, Michael. And can I stick with that cap rate comment that you made. Obviously, you're in a select targeted set of markets. But with the comment that the cap rates on transactions would be below kind of what the market is expecting right now, do you have a sense of how much cap rates have moved in your specific markets?

Michael S. Gamzon INDUS Realty Trust, Inc. – CEO, President & Director

Yes, I think, akin to that comment, it's really hard to pick a number because it's sort of -- there's so few deals. They just feel almost your cherry picking. I can give you an example. In Charlotte, there was a nice portfolio located near the airport. It had 3.5 years of weighted average lease term. We thought the rents were kind of 25% to 30% below market, about a 600,000 square foot portfolio. We've heard that's been awarded, went through kind of a multiple round process -- and so this is real time last month, and we've heard it's kind of a 4.2%, 4.3% cap rate, which I think feels pretty low. I'd say peak of the market, maybe I would have guessed that would be kind of a 3.8. So has that moved 40 basis points. That seems pretty tight compared to where debt spreads have widened and other things, but that's where that's traded.

We know there's been a closed deal in Savannah with not a lot of mark-to-market and 5 years of lease term that traded at a 4.25% Again, it's not a market we're in. We've mentioned in the past, we look at it, so we track it a little bit. That feels pretty low. There is a deal kind of in the Berks County, which is kind of the Western submarket of the Lehigh Valley. We feel the core of the 2 Eastern counties. But -- this is further West. So we think it's not as good a location typically is traded wide of the Lehigh Valley, and that closed, I think, 2 months ago at 4.25%.

So it's really hard to say exactly how much things have moved. Some things that are going to have a very, very long 15 or 20-year single-tenant net lease with not a lot of bumps. That's going to be typically wider, probably 100 to 125 basis points wider. These other deals are anywhere from, call it, 25 to 75, but it's really hard to put a pin on it.

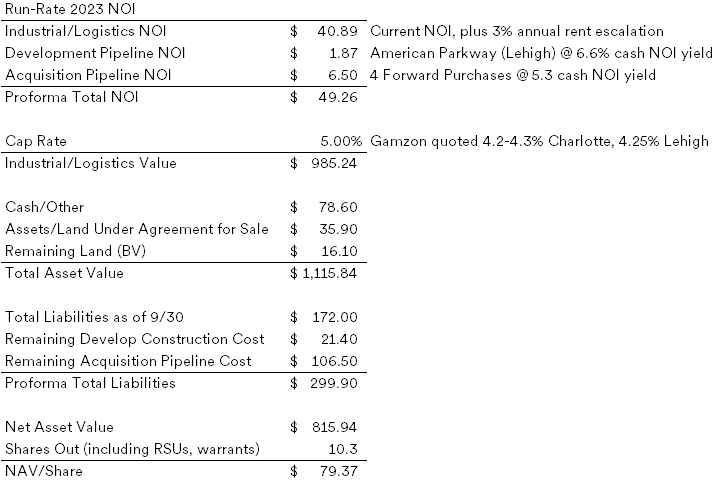

Those numbers seem difficult to believe in the current market, especially when INDT's shares were recently trading with an implied cap rate in the high 6%'s, higher than where they're currently acquiring and developing new industrial/logistics properties. With their equity trading where it is, raising future equity after completing their current pipeline (2023) seems temporarily off the table. It makes sense that private equity would come knocking on their door, so what might Centerbridge be willing to pay?

It is a little bit tricky, because of INDT's small size and growth posture, they're growing over 20% based on their acquisition and development pipeline in the next year. Relying heavily on their recent Q3 earnings supplement (particularly pages 23, 24 and 27):

I've gotten a lot of speculative M&A wrong this year so I'm not rushing to add here, but optimistic the value of INDT's real estate will be realized one way or another.

Disclosure: I own shares of INDT

But a 6 % cap rate gets a NAV/share of $ 63. Could Centerbridge borrow for much less than 6 %? Like much of CRE industrial properties seem to be in a bit of a bubble. I owned the stock and it did very well but I sold in May at about $ 67 earlier because it seemed a bit overpriced.

ReplyDelete6% is too high of a cap rate, there are other buyers below that. The 10 year is back down to 3.7%, I'm sure they could borrow on this asset base below 6%. Worth pointing out, the average age of these properties are pretty new, mark-to-market rent is ~20% below market according to management. The big public comps are mostly below 5% implied cap rates, PLD is 4.3%, REXR 4.1%, EGP 4.7%.

DeleteGood call, at least on the initial bid. I still think the price is too low.

DeleteCongrats/well done/thank you!

ReplyDeleteThanks, although I think the price is too low. Hopefully this brings forward other bidders.

DeleteA nice call. But the (current) offer of $ 65 is close to a 5 % cap rate I used (so far anyway). However a year ago Cube Smart bought LAACO (L A Athletic Co) for its public storage units at a cap rate of some 2 % so who knows what people will do.

ReplyDeleteThe LAACZ deal is almost certainly what drove OJOC price way up too (admittedly on volume of like 1000 shares over the past year). People love that scarcity value/perception of quality!

DeleteI didn't run the math on current numbers, but might be 5% cap if you don't give them credit for the pipeline, free rent rolling off, stabilization, etc. Those don't seem too high of a hurdle that they should be excluded.

DeleteBasically, for this to work for a buyer, that buyer has to be positive on at least 2 of 3 of go-forward interest rates, go-forward cap rates, and company-specific elements. I imagine Centerbridge is positive on all 3 (and with good reason, I'd say, especially on the 3rd), but it also makes me wonder who else might be on buyers' radar. First thought was PLYM, though they are a very different beast and I suspect one that's not as exciting.

DeleteI mostly agree, a bit disappointed in the $65 offer, not sure that bid/ask spread can be met in the middle if that is their opening offer. Kind of a long way to $75 or something like that. Maybe Centerbridge is just trying to put it into play. We'll see. I don't think I'd initiate a position based on this offer if I didn't already own it.

DeleteIt's interesting because they have a rep as distressed buyers, though of course they're more rounded than that. I imagine they see a chance to be opportunistic, and are especially interested in the pipeline here. In January they raised their bid for Aareal by ~6% after the first offer failed; the 2nd failed too. Not sure any of that is particularly dispositive. I am a little more inclined to add to my (very small) position, or likelier buy a few calls if I can get them cheaply.

DeleteOops! I meant a 6 % cap rate.

ReplyDeleteWhere do you get $40.89M of NOI - stated current NOI on Pg 22 of their investor presentation is $35.7M

ReplyDeleteI'm including the roll off of free rent, stabilization of the one property that is not fully occupied and a 3% escalator for next year, I don't think any of those are really a stretch. I'm attempting to come up with the run-rate NOI once their development/acquisition pipeline is executed in the next couple quarters.

Deletethat makes sense - thanks!

DeleteDo you still think they will raise the offer/ will be outbid?

ReplyDeleteNothing has really changed since the bid, I don't think $65 is going to get it done. Maybe Centerbridge was just trying to put it in play or goose up the share price before year-end, either way, it likely forced INDT's board to talk to advisors, see if there's other interest for the company, etc. That whole process takes months.

Deletehttps://www.sec.gov/Archives/edgar/data/1037390/000110465923024059/tm237508d1_ex99-1.htm

ReplyDeleteOnly $67. I was way wrong, need to adjust to the new rate environment.

STAG recently commented they are seeking deals between 5.75 and 6.5 cap rate. Seems like private market valuations for industrial/logistics properties is stabilising at ~6%

ReplyDelete