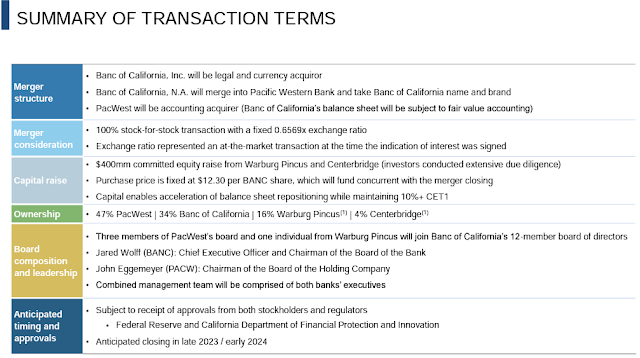

Banc of California (BANC) and PacWest's (PACW) merger is a bit old news at this point, but initial excitement has worn off and shares are now priced below $12.30/share, where PE firms Warburg Pincus and Centerbridge are making their PIPE investment (originally at a 20% discount, it will close with the merger). This is less of a short-term special situation trade and more a medium-to-long term investment as we wait for the skies to clear in the regional bank industry and bet on the merged bank extracting a massive amount of synergies. The merger is a complicated transaction, the basic terms are below, all of this is designed to clean up the larger distressed PacWest:

The accounting here will be a bit quirky, in an acquisition or a merger, a bank needs to mark-to-market the assets of the acquired bank on their balance sheet. As everyone is well aware, where current rates are, banks have large unrealized losses that aren't included on their balance sheet in both the loans held for investment and securities held-to-maturity portfolios. Since Banc of California is in relatively better shape, PacWest will be the acquirer here so that BANC's assets are marked-to-market rather than PACW's. There's a lot of moving pieces here (BANC is selling their residential mortgage and multi-family portfolios among other asset sales to plug the wholesale funding problem), but in the interest of brevity, Warburg Pincus and Centerbridge's investment was designed to plug the capital ratio hole created by this mark-to-market merger accounting, keeping the merged bank's capital ratios in the healthy 10+% CET1 range.

My high level core thesis here is mainly two fold:

- Pre-regional bank crisis, bank mergers were highly scrutinized. Back in the summer of 2021, President Biden released an executive order that "encourages DOJ and the agencies responsible for banking (the Federal Reserve, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency) to update guidelines on banking mergers to provide more robust scrutiny of mergers." What this meant in practice, banks had to convince regulators/politicians to approve a merger by limiting branch closures and job cuts, make grants into the community, etc. That's not the case here, regulators are rolling out the red carpet to ensure that the contagion doesn't spread. The two parties are guiding to only a six month merger timeline as they've already previewed this deal with regulators. While they'll be careful not to explicitly say it, but the two banks have a ton of geographical overlap that will get rationalized in the coming year or two post closing, likely blowing past their projected synergies.

- Banc of California previously had a reputation as a bit of a renegade fast growing bank under Steven Sugarman (brother of SAFE's Jay Sugarman), they entered a lot of risky lines of business and even plastered their name on a new soccer stadium in LA for $15MM/year, quite the marketing expense for a small regional bank. However, four plus years ago Sugarman was pushed aside, in came Jared Wolff to lead the bank, he grew up at PacWest (with a stop in between at City National, another LA bank) and knows it and its management team very well. Wolff shed many of the risky lines of business, ditched the stadium licensing deal, instead focused on being a community commercial bank. BANC has performed reasonably well since, trading between 1.1-1.4x book value. This is a bit of a jockey bet that he can draw on both his experience turning around BANC and being the former president of PACW to merge these two organizations optimally.

- This deal doesn't solve two issues the market has been worried about, geographic concentration and deposit concentration risk, the combined bank will still be commercial focused (lacking significant retail deposits) and in California. But maybe neither should be a concern going forward? Market could be fighting the last war, but something I've been thinking about and don't have a strong rebuttal.

- One of BANC's pitches is there is a void to fill because many of the largest California headquartered banks have either failed or been merged away in recent years. I don't entirely buy that as the money center banks have a large presence in California, banking is a relative commodity, while relationship community banking can be a good profitable niche, I struggle thinking there's massive growth opportunity here. This is a merger execution story, not a growth one.

- Proforma, 80% of deposits will be insured, like to see that a bit higher, but this is a commercial focused bank. They'll still be a pretty small bank with only 3% deposit share in southern California.

- Outside of the current bank environment risks, this situation does carry a fair amount of execution risk. I've been apart of a few acquisitions before, things always take longer and are hairier than it appears to outsiders, need to have some patience.

Disclosure: I own shares of BANC and PACW

Hi Mike, Thanks for the writeup. Have you considered looking at PACWP. THanks.

ReplyDeleteI did look at it, probably attractive for lower risk investors, but I have a pretty high hurdle and a high hurdle to get involved in preferred stock. But it does look attractive.

DeleteI think PACWP is pretty interesting. Decent likelihood it trades for a lot closer to par upon consummation of the merger not incredible downside given the merger. The common is pretty interesting too but there are many banks that are similarly cheap. Probably a couple of years out many regional banks will trade for 1.2-1.5x tangible book. $CUBI, OPBK, PCB, NECB etc. (maybe throw in the ECIP banks too) the question is when and how much to buy. They’re cheap now but people will continue to freak out whenever the 10 year goes up marginally. A couple of the banks i mentioned have tried to transition to mostly floating rate loans. I’m going with a more basket approach, though I like $CUBI more because everyone hates its guts irrationally.

DeleteLots of small cap bank mergers are pretty interesting the spreads are high and timing is, for similar reasons you mentioned, likely to be lower than usual.

ZYNE CVR merger is interesting because the first milestone is very likely to payout because it’s simply completing the phase 3 trial. Then you get an additional ~$2.3 upside. Have no idea of the science.

SSNT a decent consulting business with a potential for $1.5 dividend from a merger as well as 3% of a speculative shitco while maintaining 100% ownership of the original business.

Thanks. Appreciate the ideas, especially the "no idea of the science", sounds like my kind of trade.

DeleteCurious if anyone has thoughts on the IDFB / BAWAG AG merger arb setup (VIC write up, lots of other ink spilled on it online). Feels like an attractive setup to me, but I am not a bank expert.

ReplyDeleteBAWAG management on the most recent conference call seemed bullish still on the purchase and liked Peak’s results. (Conference call was just earlier this month). It’s very small compared to the market cap of BAWAG. Will be interesting to see if they use Peak as a platform for other acquisitions. Downside is probably 20%. Likely goes through.

DeleteEver looked at CNDT? Mkt cap is ~$650M and net debt is $935M (including $120M of preferred stock) for an EV of ~$1.6B. From what I’ve looked into, there’s 4 main assets: (1) BenefitWallet (worth probably >$350M based on HQY acquisition of Fifth Third Bank’s $477M HSA portfolio for $61M or $0.13/$1.00 of AUM), (2) Strataware (worth probably >$200M based on acquisition by XRX in FY14 for $225M), (3) Government Services (includes EBT contractor and MMIS vendor businesses doing $330M in TTM-adj EBITDA and if you allocate 30% of $270M of corporate overhead adj EBITDA based on its sales contribution, then that’s $250M in carve-out EBITDA, using a government contractor multiple of 10-12x, then it’s worth $2.5B-$3.0B), and (4) Transportation (mix of transport agency contractor businesses that has been experiencing earnings declines from contracts rolling off that mgmt is saying will improve in 2H24, w/ $60M in adj EBITDA and assumed $20M in corporate overhead, that’s $40M in EBITDA, although I feel this segment’s earnings should improve going forward, at 8x multiple it’s worth $320M, most write-ups assign much more value to this segment). So that’s total ~$3.4B-$3.9B in asset value against $1.6B of EV, of which $0.9B is net debt. I think the government services business is under-appreciated by the market right now. Management is focused on divestitures of $500M-$700M (I trust them as Carl Icahn owns 18% of s/o and holds 3/8 board seats) in the near term and that’ll offset some of the risks related to poor FCF conversion and rising interest burden due to floating rate debts.

ReplyDeleteThanks. I appreciate the idea. I looked at them at the time of their spin, I worked in some adjacent projects/industries to CNDT, they had a poor reputation at the time, but that might have changed. I'll revisit, thanks.

DeleteIt’s particularly interesting right now due to the attractive environment for a BenefitWallet sale. From VIC, every 25bps of rate hikes is a $7M increase to EBITDA. Pre-COVID BW was doing $40M in EBITDA when rates were ~1.5-2%. Now they’re 5.4%, so EBITDA would be >$100M. HQY trades at 18x fwd EBITDA. They could pay 5-7x and that’d be around management’s divestiture target ($500-$700m).

DeleteThanks - I have some time later this week, I'll revisit it. I appreciate your thoughts!

DeleteKind of expected a lower bid on this. BW transfer to HQY for $425M.

DeleteNow EV is ~$1.2B. Gov Pmts + Transpo break-up EBITDA >$300M. So the business is now at 4x EBITDA. Strataware could be next, then EV would probs be ~$1B and 3.3x EBITDA. This is from 2021: http://www.joepaduda.com/2021/09/22/consolidation-in-work-comp-services-comments-on-conduent/

DeleteThis is a precedent transaction for Strataware:

http://www.joepaduda.com/2013/09/09/mitchell-acquired-whats-next/

Strataware sold for 9.5x EBITDA/$240M on May 6

ReplyDelete