Magenta Therapeutics (MGTA) ($39MM market cap) is a member of my broken biotech basket, I'm bringing it forward again to highlight the opportunity for shareholders to vote down the proposed reverse merger with privately held Dianthus Therapeutics. In MGTA's S-4, the company strongly hints that if the deal is not approved, a dissolution and liquidation is on the table:

If the merger is not consummated, Magenta’s board of directors may decide to pursue a dissolution and liquidation. In such an event, the amount of cash available for distribution to its stockholders will depend heavily on the timing of such liquidation as well as the amount of cash that will need to be reserved for commitments and contingent liabilities.

There can be no assurance that the merger will be completed. If the merger is not completed, Magenta’s board of directors may decide to pursue a dissolution and liquidation. In such an event, the amount of cash available for distribution to its stockholders will depend heavily on the timing of such decision and, with the passage of time the amount of cash available for distribution will be reduced as Magenta continues to fund its operations. In addition, if Magenta’s board of directors were to approve and recommend, and its stockholders were to approve, a dissolution and liquidation, Magenta would be required under Delaware corporate law to pay its outstanding obligations, as well as to make reasonable provision for contingent and unknown obligations, prior to making any distributions in liquidation to its stockholders. As a result of this requirement, a portion of its assets may need to be reserved pending the resolution of such obligations and the timing of any such resolution is uncertain. In addition, Magenta may be subject to litigation or other claims related to a dissolution and liquidation. If a dissolution and liquidation were pursued, Magenta’s board of directors, in consultation with its advisors, would need to evaluate these matters and make a determination about a reasonable amount to reserve. Accordingly, holders of its common stock could lose all or a significant portion of their investment in the event of liquidation, dissolution or winding up.

Included in the S-4 is also a management prepared liquidation analysis (the distribution estimate here assumes a May or June 2023 distribution, clearly that's not a realistic timeline, additional liquidation costs will be incurred if MGTA does end up down that road):

In light of the foregoing factors and the uncertainties inherent in estimated cash balances, stockholders are cautioned not to place undue reliance, if any, on the Liquidation Analysis.

The below summary of the Liquidation Analysis is subject to the statements above, and it represents Magenta management’s estimates of Magenta’s cash which may be distributed to stockholders as permitted under applicable law pursuant to a plan of dissolution.

Key assumptions underlying the Liquidation Analysis included (i) that the entire distribution of Magenta’s net cash would be made in either May 2023 or June 2023, (ii) that Magenta would have approximately $65.2 million and $63.9 million of net cash as of May 2023 and June 2023, respectively, after deducting costs and expenses, including legal fees, the fees payable to Magenta’s strategic financial advisor, accounting fees, employee retention bonuses, severance and benefits, insurance expenses and other transaction-related costs, with no adjustments for taxes; (iii) that these costs and expenses were forecasted to total approximately $11.8 million assuming the closing of a liquidation in each of May 2023 and June 2023; and (iv) approximately 60.7 million total shares outstanding as of April 27, 2023. The analysis resulted in an estimated cash distribution per share in May 2023 and June 2023 of $1.07 per share and $1.05 per share, respectively.

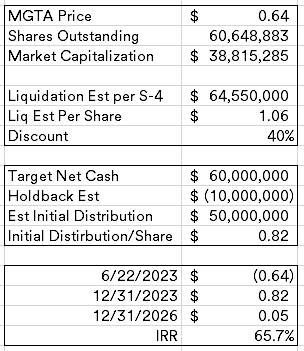

Today, shares trade for $0.64 per share, well below management's liquidation estimate. There's a reasonable presumption a liquidation would indeed follow a "no" vote to the merger, per the merger agreement, MGTA would be required to pay a termination fee of $13.3MM (huge in comparison to their cash balances or market cap) if MGTA enters into another merger within 12 months.

Termination Fees Payable by Magenta

Magenta must pay Dianthus a termination fee of $13.3 million if (i) the Merger Agreement is terminated by Magenta or Dianthus pursuant to clause (e) above or by Dianthus pursuant to clause (f) above, (ii) at any time after the date of the Merger Agreement and prior to the Magenta special meeting, an Acquisition Proposal with respect to Magenta will have been publicly announced, disclosed or otherwise communicated to the Magenta board of directors (and will not have been withdrawn), and (iii) in the event the Merger Agreement is terminated pursuant to clause (e) above, within 12 months after the date of such termination, Magenta enters into a definitive agreement with respect to a subsequent transaction or consummates a subsequent transaction.

A liquidation would be their only realistic option, 12 months is a long time to wait it out for a cash burning biotech with no pipeline (they sold all their assets in April). In order to close the deal, MGTA needs a majority of the votes cast to vote in favor of the merger (edit: they need a majority of the shares outstanding), the support agreement only has 6.9% of the shares, leaving quite a bit of ground to cover. Tang Capital Management owns just under 10% and presumably is the Investor named in the background section of the S-4 who proposed a cash tender offer:

Between March 1, 2023 and March 28, 2023, a stockholder of Magenta (the “Investor”) made several unsolicited inquiries to Stephen Mahoney, the President, Chief Financial and Operating Office of Magenta, to inquire whether Magenta would have an interest in the Investor proposing a cash tender offer for Magenta at a discount to its current cash position. No specific proposal, terms or valuation were discussed during this conversation, or any subsequent conversation between the Investor and representatives of Magenta.

It is unlikely that Tang would vote in favor of the reverse merger at this point, given the current discount to cash. I'm guessing it will be challenging for management to get the 50% of the vote necessary, but as we've seen in other microcaps, getting investors to vote at all could be an issue. A non-vote here doesn't impact the vote one way or another, likely benefitting management.

MGTA's target net cash position at the time of closing (Q3) per the merger agreement is $60MM, if we assume that the vote fails and MGTA pursues a liquidation, let's guess that they holdback $10MM for additional winddown expenses or contingencies.

Above is my potential IRR math, I'm assuming an initial distribution by year end and then a small one ($3MM of the $10MM holdback) in 3 years. In addition, the company did sell their pre-merger assets in April, $20MM in combined milestone payments are in play too, but I'm assuming those are worthless. The merger vote hasn't been set yet, but I would expect it in early-mid Q3. I bought more recently.

Disclosure: I own shares of MGTA

Thanks for this one, MDC.

ReplyDeleteHow should we think about the value in a deal closes scenario?

I followed your lead into Imara (and did very well) but sold when the reverse merger was announced. The market clearly loved that reverse merger with Enliven (I should have held longer). In this case, the market seems to dislike/distrust the Dianthus merger.

You do a nice job of showing the deal breaks scenario above, but I'm curious if you have any view on what the deal closes scenario is worth.

Thanks

That is the wildcard, as I probably show time and time again, I'm not a scientist and have no clue how to value a going concern biotech. The merger valued MGTA at $80MM ($20MM for the shell, $60MM for the target net cash), the other investors are providing a PIPE alongside the merger. But who knows where it would trade in the meantime, that's certainly the risk.

DeleteBoth Enliven and pro forma Dianthus claim to expect to have enough cash to operate through sometime in 2026. There is large and constant dilution occurring with biotechnology companies, so I think investors appreciate being able to see if the companies have a real product, before more cash will be required.

DeleteMDC, this was a favorable development to the MGTA story. I'm wondering how do you discover these failed biotechs on the verge of corporate restructuring so quickly? Do you have a RSS feed on the SEC website for certain filings? I regularly come across a slew of biotechs when I run a screener for cash shell like companies but it's very hard to sift through each one of them and check whether they are willing to raise the white flag or simply continue burning more capital and diminishing the margin of safety.

ReplyDeleteI haven't found one fail safe way of discovering these, it is a combination of things, heavy use of Google alerts, screening for negative enterprise value and tracking SEC filings on those (I use BamSEC), and then people in my network are doing similar things and share with me when they find something interesting.

DeleteDo you see the mid .60s as a reasonable value should the merger be approved? Also any thoughts on WHLRD as we get closer to the redemption date?

ReplyDeleteSimilar thought as the first question, merger values MGTA at ~$1.30 (which is presumably why the board recommended it over at liquidation), so the market is valuing Dianthus at half that via MGTA. Pretty big discount, but again, I have no idea how to value Dianthus or evaluate its pipeline.

DeleteI don't follow WHLRD closely, never owned it. I couldn't get past management being outwardly hostile to the preferred. As a general rule, if management can screw preferred shareholders, they will.

Took a quick read of the DMA - my view is they need a majority of outstanding shares, not majority of votes. So ppl who don't show up to vote hurt mgmt / are effective no votes against the merger

ReplyDeleteYou're right. I was just looking at Proposal 1, but Proposal 2 you need a majority of the outstanding shares. Both are required to pass as a condition of the merger:

DeleteRequired Vote

The presence at the Magenta special meeting of the holders of a majority of the shares of Magenta common stock outstanding and entitled to vote at the Magenta special meeting is necessary to constitute a quorum at the meeting. Abstentions and broker non-votes, if any, will be counted towards the presence of a quorum. The affirmative vote of a majority of the votes properly cast by the holders of Magenta common stock, assuming a quorum is present, is required for approval of Proposal Nos. 1, 5 and 6. The affirmative vote of a majority of the outstanding shares of Magenta common stock entitled to vote at the Magenta special meeting is required for approval of Proposal Nos. 2 and 3. With respect to Proposal No. 4, directors are elected by a plurality of the votes properly cast at the Magenta special meeting, and the three nominees for director receiving the highest number of affirmative votes properly cast will be elected. Each of Proposal No. 1 and Proposal No. 2 is a condition to completion of the merger. Therefore, the merger cannot be consummated without the approval of Proposal Nos. 1 and 2.

Hi MDC, my reading of the docs was that the termination fee would be payable even in the event of a liquidation. The merger docs define the trigger for the termination fee to be a "subsequent transaction", which is defined as an "acquisition transaction" with the threshold increased from 20% to 50%.

ReplyDeleteHere is the definition from the merger docs:

“Acquisition Transaction” means any transaction or series of related transactions (other than the Magenta Legacy Transaction) involving:

(a) any merger, consolidation, amalgamation, share exchange, business combination, issuance of securities, acquisition of securities, reorganization, recapitalization, tender offer, exchange offer or other similar transaction: (i) in which a Party is a constituent Entity, (ii) in which a Person or “group” (as defined in the Exchange Act and the rules promulgated thereunder) of Persons directly or indirectly acquires beneficial or record ownership of securities representing more than 20% of the outstanding securities of any class of voting securities of a Party or any of its Subsidiaries or (iii) in which a Party or any of its Subsidiaries issues securities representing more than 20% of the outstanding securities of any class of voting securities of such Party or any of its Subsidiaries; provided, however, in the case of the Company, the Company Pre-Closing Financing shall not be an Acquisition Transaction; or

(b) any sale, lease, exchange, transfer, license, acquisition or disposition of any business or businesses or assets that constitute or account for 20% or more of the consolidated book value or the fair market value of the assets of a Party and its Subsidiaries, taken as a whole.

I suspect that (b) may cover a liquidation scenario, as the company would be "disposing" of > 50% of its assets.

I might be wrong, but I think it's worth considering. At current prices, it still probably works out OK.

Hmm, yeah there's a lot of poor drafting. When I started looking at this, I thought the agreement read that even if the deal is voted down, then MGTA owes a termination fee. I see what you're saying there, "disposing" does seem to be the key word. But the CFO/General Counsel did confirm that the intention is if they liquidate, they don't owe the termination fee. Maybe this ends up getting litigated which wouldn't be good for shareholders.

DeleteThanks for the response. So did MGTA’s CFO/counsel confirm that in the docs? Or did you speak to them?

DeleteI didn't speak with them directly, but a reader I respect did. They confirmed verbally.

DeleteOK, thanks for clarifying that. If that’s the case, maybe there will be no fee due after all. I guess we’ll have to wait and see. I tried to contact MGTA’s IR but I didn’t get a response myself.

DeleteNot a lawyer but believe there is also a time window on that language so even if there was a dispute from the Dianthus side about whether a liquidation triggers the 13.3mm fee one easy out would be just waiting a year, with 1y treasuries now earning 5.25% on the full cash balance that would be unfortunate but less impactful than when rates were 0. My impression was that language is there to prevent a Tang-style counter-offer or alternate deal, not a liquidation so isn’t a problem if deal isn’t voted down. Improved deal terms seem only viable path to avoiding liquidation, maybe like TALS where a large portion of the MGTA entity’s cash is dividended instead of reinvested.

DeleteTermination Fees Payable by Magenta

Magenta must pay Dianthus a termination fee of $13.3 million if (i) the Merger Agreement is terminated by Magenta or Dianthus pursuant to

clause (e) above or by Dianthus pursuant to clause (f) above, (ii) at any time after the date of the Merger Agreement and prior to the Magenta special

meeting, an Acquisition Proposal with respect to Magenta will have been publicly announced, disclosed or otherwise communicated to the Magenta

board of directors (and will not have been withdrawn), and (iii) in the event the Merger Agreement is terminated pursuant to clause (e) above, within 12

months after the date of such termination, Magenta enters into a definitive agreement with respect to a subsequent transaction or consummates a

subsequent transaction.

Magenta must reimburse Dianthus for expenses incurred by Dianthus in connection with the Merger Agreement and the transactions contemplated

thereby, up to a maximum of $1.5 million if Dianthus terminates the Merger Agreement pursuant to clause (h) above.

Management won't necessarily know if there is a dispute until after the fact. They could broach the subject and ask for permission to liquidate upfront, which could be denied, or make the liquidation and risk litigation. And asking upfront only increases the risk because you are tipping them off you are worried. I don't think that is the intent of the agreement but its pretty clear/muddy with the word "disposition" listed in (b). Disposition: the action of distributing or transferring property or money to someone, in particular by bequest.

DeleteOther than Tang, with these guys as top holders what are thoughts on the shareholder vote now that it's clear it's 50% of outstanding? 44% total here

ReplyDeleteLion Point Capital LP 7.52

Citadel Advisors LLC 6.74

Atlas Venture Life Science Advisor 6.25

Atlas Venture Fund X LP 6.25

Alphabet Inc 5.51

Verition Fund Management LLC 3.62

Vanguard Group Inc/The 3.25

Western Standard LLC 2.37

Gardner Jason 1.56

TCW Group Inc/The 1.24

The deal was announced in May, many of these shareholders might not own it any longer as most of these ownership levels are as of 3/31.

DeleteThis merger was announced 3-May. If any large shareholders objected, I would think they would file a 13D by now. Try to stop the expense of the merger. These are biotechnology investors, foremost. Perhaps they actually like the merger and its terms.

ReplyDeleteMaybe you're right. But the price action seems to tell a different story, current price is way below the implied deal price, which kind of tells you that traditional biotech investors aren't into the target. And this might be too small for your typical activist fund. We'll see what happens, but I think its fairly clear that investors should vote it down, whether they will, hard to say.

DeleteSometimes the price of a reverse merger candidate will not go up until after the merger is officially consummated. But obviously it’s not something to count on.

DeleteMDC - What do you mean by "implied deal price." The pro forma price based on the "concurrent financing," or something else? Thanks.

DeleteThe reverse merger ascribed $80MM in value for MGTA in the exchange ratio, take it with a grain of salt, but it is well above the current share price.

DeleteThe 8 biotech investors are buying $70 million newly issued shares at the same valuation. So I don't understand the comment that "traditional biotech investors aren't into the target." Are they not reputable investors?

DeleteThere are more than 8 biotech investors correct? At least public market investors are not willing to pay the same price as the PIPE investors. Any other biotech investor is free to pay $0.70/share and vote yes for the deal if they believed in the ascribed valuation, it would be a home run trade, but not enough are clearly.

DeleteYes, I do think there are more than 8 biotech investors, in this world.

DeleteThey may not be looking hard at this $40 million company. But maybe you are correct, they have all spent time analyzing it, and reached the same conclusion.

I apologize, that came across rude. I could very well be wrong about all this, often am, the merger might go through and maybe that's best for long term shareholders including the PIPE investors.

DeleteWhat hasn't been discussed yet is the possibility that Dianthus will sweeten the pot a little (similar thing happened with the Sesen / Carisma deal). I.e. if the deal is about to fail it could be that they throw in a small cash component and/or improve the exchange ratio a bit.

ReplyDeleteIn any case I'm not so sure that mangement will throw in the towel immediately if the deal is about to fail. Not sure if that is a good thing or not. Obviously a deal sweetener would be nice but at the same time I think there's a risk that the timeline gets longer and/or that things end up in court. In both cases the IRR would drop and the cash balance would go down quickly as well.

I'm on the sidelines for now.

True, I wouldn't be surprised if they recut the deal to include a special dividend to MGTA shareholders. Seems like most of the recent deals include this, see TALS.

DeleteWhat's the word on the vote?

ReplyDeleteIt passed and wasn't particularly close.

Deletesurprising...I have noticed a lot of odd voting...passive owners I guess

DeleteWhat do you think it's worth now that the deal is approved? Thanks!

ReplyDeleteHopefully others can chime in, I don't know what it is worth now, don't have enough expertise in the science to really comment.

DeleteDNTH has rallied nicely in the last few days post merger closing. I sold this morning, closing this one out as my thesis was wrong, thankfully was able to exit with a small gain in the end.

ReplyDelete